Liabilities represent the financial obligations or debts a company or organization owes to others. They are a crucial component of both a company’s balance sheet and a nonprofit’s balance sheet, reflecting loans, accounts payable, and other debts. Unlike assets, which provide future economic benefits, liabilities signify future sacrifices of economic benefits. Proper management of liabilities is essential for maintaining financial stability and solvency.

What Is Liability?

Liability refers to a company’s legal financial debts or obligations that arise during business operations. These obligations must be settled over time through the transfer of money, goods, or services.

How Liabilities Work

Liabilities are financial obligations a business must settle, playing a critical role in its financial structure. Financing leasing allows companies to use assets without immediate full payment, spreading costs over time. Finance, including loans and credit, enables businesses to invest and grow. Understanding finance essentials, such as managing liabilities, is crucial for business success, ensuring cash flow stability and financial health.

Types of Liabilities

1. Current Liabilities

Current liabilities are obligations that a company must settle within one year. They are essential for assessing a company’s short-term liquidity and financial health. Managing current liabilities effectively ensures that a business can meet its short-term obligations without facing cash flow issues. Key examples include:

- Accounts Payable: Money owed to suppliers for goods or services received but not yet paid for.

- Short-Term Loans: Loans that need to be repaid within a year.

- Accrued Expenses: Expenses that have been incurred but not yet paid, such as wages, interest, and taxes.

2. Non-Current Liabilities

Non-current liabilities are long-term financial obligations due after one year. These liabilities are vital for understanding a company’s long-term financial commitments and its ability to finance large projects or investments. Effective management of non-current liabilities helps in planning for future growth and stability. Key examples include:

- Long-Term Loans: Loans that are due for repayment over a period longer than one year, often used for significant investments like purchasing property or equipment.

- Bonds Payable: Debt securities issued by a company to raise capital, which must be repaid over a period longer than one year.

- Deferred Tax Liabilities: Taxes that are accrued but not yet payable, representing future tax payments due to temporary differences between accounting income and taxable income.

3. Contingent Liabilities

Contingent liabilities are potential obligations that may arise depending on the outcome of a future event. These liabilities are not certain and are only recognized when it is probable that a loss will occur and the amount can be reasonably estimated. Proper assessment and management of contingent liabilities help in risk management and financial planning. Key examples include:

- Lawsuits: Potential legal obligations that may arise from ongoing litigation. If a lawsuit is likely to result in a loss, the company needs to estimate and disclose the potential liability.

- Product Warranties: Future costs that a company may incur to repair or replace products under warranty. Companies must estimate the expected warranty costs and recognize them as liabilities.

- Environmental Cleanup Costs: Potential costs associated with environmental damage for which a company may be responsible. These liabilities depend on regulatory actions or discovered contamination.

Example of Liabilities

- Accounts Payable: Money owed to suppliers for goods and services received.

- Loans Payable: Amounts borrowed from financial institutions or other lenders.

- Credit Card Debt: Outstanding balances on business credit cards.

- Mortgages: Loans secured by real estate property.

- Accrued Expenses: Expenses incurred but not yet paid, such as wages, rent, and utilities.

- Deferred Revenue: Money received in advance for services or products to be delivered in the future.

- Bonds Payable: Long-term debt securities issued to investors.

- Taxes Payable: Taxes owed to the government that are due within the year.

- Interest Payable: Interest expenses that have been incurred but not yet paid.

- Salaries Payable: Wages owed to employees for work performed.

- Warranty Liabilities: Estimated costs of repairing or replacing products under warranty.

- Dividends Payable: Dividends declared by the company but not yet paid to shareholders.

- Lease Liabilities: Obligations under lease agreements for property or equipment.

- Notes Payable: Written promises to pay a specified amount of money at a future date.

- Unearned Revenue: Money received for goods or services that have not yet been delivered or performed.

- Pension Liabilities: Obligations to pay retirement benefits to employees.

- Customer Deposits: Funds received from customers as a security deposit or advance payment.

- Legal Settlements Payable: Amounts owed as a result of legal judgments or settlements.

- Deferred Tax Liabilities: Taxes owed for income that has been earned but not yet taxed.

- Utility Bills Payable: Outstanding bills for utilities like electricity, water, and gas.

Current Liabilities

1. Accounts Payable: When a company purchases goods or services on credit from suppliers, the amount owed becomes accounts payable. For example, a retail store orders inventory worth $10,000 from a supplier, agreeing to pay within 30 days. This $10,000 is recorded as a current liability.

2. Short-Term Loans: These are loans that need to be repaid within a year. For instance, a company may take out a $50,000 short-term loan to cover immediate expenses. The entire $50,000 is classified as a current liability.

3. Accrued Expenses: Expenses that have been incurred but not yet paid, such as wages and utility bills. For example, if a company owes $5,000 in wages to its employees at the end of the month, this amount is an accrued expense and a current liability.

Non-Current Liabilities

1. Long-Term Loans: Loans with repayment terms extending beyond one year. For example, a business secures a $200,000 loan to purchase new machinery, with repayments scheduled over five years. The outstanding balance of this loan is recorded as a non-current liability.

2. Bonds Payable: When a company issues bonds to raise capital, the amount owed to bondholders is recorded as bonds payable. For example, if a company issues $1 million in bonds payable over 10 years, this amount is a non-current liability.

3. Deferred Tax Liabilities: These arise from differences in the timing of income recognition between accounting rules and tax laws. For example, if a company has deferred tax liabilities of $15,000 due to accelerated depreciation methods for tax purposes, this amount is recorded as a non-current liability.

Contingent Liabilities

1. Lawsuits: If a company is sued for $100,000 and the legal team estimates a high probability of losing, this amount is recorded as a contingent liability. The actual liability will depend on the lawsuit’s outcome.

2. Product Warranties: A company offering a warranty on its products must estimate the cost of potential repairs or replacements. For example, if a company expects $20,000 in warranty claims over the next year, this amount is recorded as a contingent liability.

3. Environmental Cleanup Costs: If a manufacturing company anticipates spending $50,000 on environmental cleanup due to regulatory requirements, this potential expense is a contingent liability.

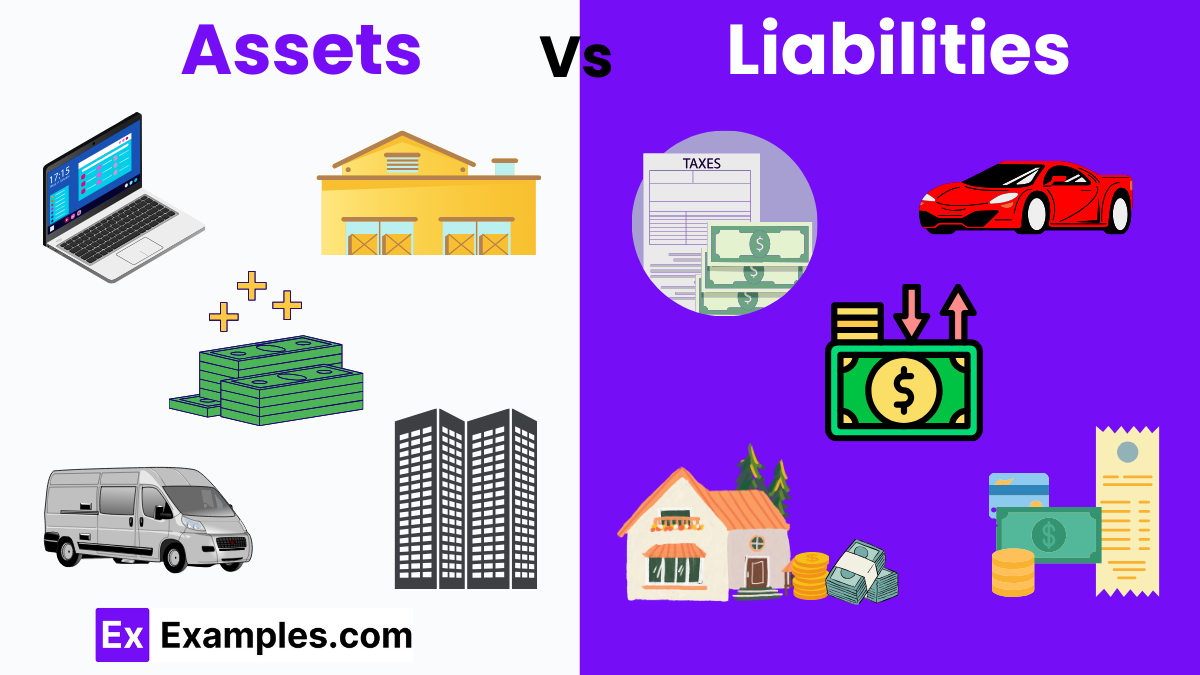

Liabilities vs. Assets

| Aspect | Liabilities | Assets |

|---|---|---|

| Definition | Financial obligations or debts a company owes to others | Resources owned by a company that provide future economic benefits |

| Examples | Accounts payable, short-term loans, accrued expenses, long-term loans, bonds | Cash, inventory, property, equipment, investments, accounts receivable |

| Current vs. Non-Current | Current liabilities (due within 1 year) and non-current liabilities (due after 1 year) | Current assets (easily converted to cash within 1 year) and non-current assets (long-term) |

| Impact on Balance Sheet | Appear on the right side of the balance sheet, indicating financial obligations | Appear on the left side of the balance sheet, indicating owned resources |

| Effect on Financial Health | High liabilities can indicate financial risk and impact creditworthiness | High-value assets can enhance a company’s financial stability and creditworthiness |

| Management Focus | Managing repayment schedules, reducing debt, and maintaining liquidity | Efficiently utilizing and investing in assets to generate revenue |

| Role in Financial Ratios | Used in ratios like debt-to-equity, current ratio, and quick ratio | Used in ratios like return on assets, asset turnover, and current ratio |

Liabilities in corporate finance essentials refer to debts and financial obligations a company must settle, crucial for understanding its financial structure and stability.

Liabilities appear on the right side of a company’s balance sheet, indicating financial obligations that must be paid off, impacting overall financial health and liquidity.

Examples of current liabilities include accounts payable, short-term loans, and accrued expenses, which are due within one year.

Non-current liabilities are long-term financial obligations due after one year, unlike current liabilities, which are due within one year.

Contingent liabilities are potential obligations depending on future events, while actual liabilities are definite financial commitments already incurred.

Understanding liabilities is vital in corporate finance to manage debt, plan financial strategies, and ensure long-term solvency and growth.

Analyzing a balance sheet helps identify liabilities by reviewing the listed financial obligations and understanding their impact on the company’s financial position.

Liabilities reduce disposable income as debts and obligations must be paid off, decreasing the amount available for personal or business spending.

Liabilities in a marketing partnership agreement outline the financial responsibilities each party must fulfill, ensuring clarity and accountability in the partnership.

A company can manage its liabilities by maintaining a balance between current and non-current liabilities, ensuring timely payments, and planning for future obligations.