Investment Decisions

The Investment Decisions are a core area essential to strategic planning and financial management. You’ll examine capital budgeting techniques, including net present value, internal rate of return, and payback period, to assess potential investments. This section covers risk analysis, cost of capital, and the evaluation of long-term financial projects. Understanding these concepts is crucial for making informed investment choices that align with corporate objectives and maximize shareholder value, key competencies for excelling in the Financial Planning and Analysis section of the exam.

Learning Objectives

In studying “Investment Decisions” for the CMA, you should learn to evaluate various types of investments by analyzing cash flows, risks, and returns to make sound financial decisions. Understand capital budgeting techniques, including net present value (NPV), internal rate of return (IRR), and payback period, and how to apply them to assess project viability. Analyze the impact of investment decisions on a company’s financial health and strategic goals. Evaluate the role of cost of capital in decision-making and explore the trade-offs between risk and return. Additionally, gain proficiency in performing sensitivity analyses to assess how changes in assumptions affect investment outcomes, preparing you to make informed, data-driven decisions.

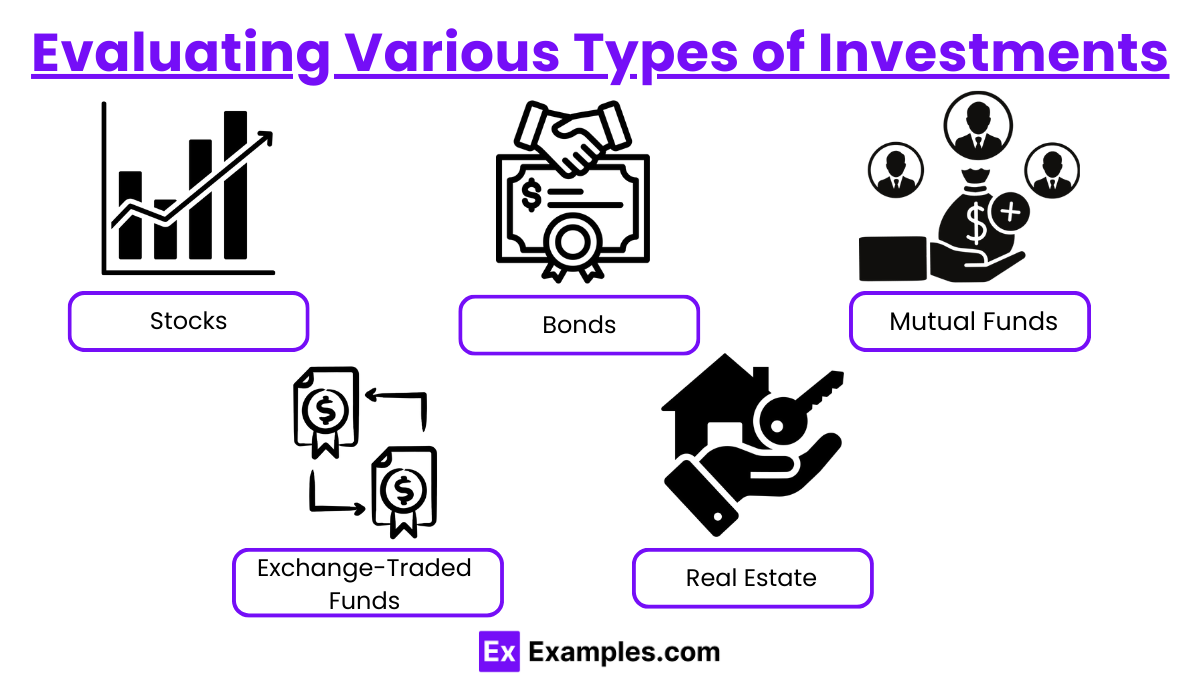

Evaluating Various Types of Investments

Investors have a wide range of investment options, each with unique characteristics, risks, and potential returns. Evaluating these options helps investors make informed choices based on their financial goals, risk tolerance, and time horizon. Here’s an overview of common investment types and what to consider for each:

1. Stocks

Stocks represent ownership in a company and allow investors to benefit from the company’s growth through price appreciation and dividends.

Characteristics:

- Potential for High Returns: Historically, stocks have offered higher returns over the long term than many other investments.

- Volatility: Stock prices can be highly volatile, influenced by market trends, economic conditions, and company performance.

- Dividends: Some stocks pay dividends, providing regular income in addition to potential capital gains.

2. Bonds

Bonds are debt securities issued by corporations, municipalities, or governments, offering regular interest payments and principal repayment at maturity.

Characteristics:

- Stable Income: Bonds provide regular interest payments, making them a steady income source.

- Lower Risk: Generally less volatile than stocks, but bond values can fluctuate with interest rate changes.

- Credit Risk: The risk that the issuer may default on payments, especially with lower-rated bonds.

3. Mutual Funds

Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets, managed by professionals.

Characteristics:

- Diversification: Allows investors to spread risk across various assets, reducing the impact of individual asset volatility.

- Professional Management: Managed by professionals, though fees may apply, impacting net returns.

- Types of Funds: Different types of mutual funds focus on stocks, bonds, or other strategies (e.g., growth funds, income funds).

4. Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds but trade on stock exchanges, offering diversified portfolios that track specific indexes or sectors.

Characteristics:

- Liquidity: ETFs can be bought or sold throughout the trading day, providing more flexibility than mutual funds.

- Low Fees: Typically lower expense ratios than mutual funds, though trading fees may apply.

- Range of Options: Available for various asset classes and sectors, including equity, bonds, commodities, and more.

5. Real Estate

Investing in real estate involves purchasing physical properties (residential, commercial, or industrial) or investing through Real Estate Investment Trusts (REITs).

Characteristics:

- Potential for Appreciation: Real estate often appreciates over time, offering capital gains potential.

- Income Generation: Rental properties generate steady income, though maintenance and management are required.

- Illiquidity: Physical real estate is less liquid, and selling property may take time and incur transaction costs.

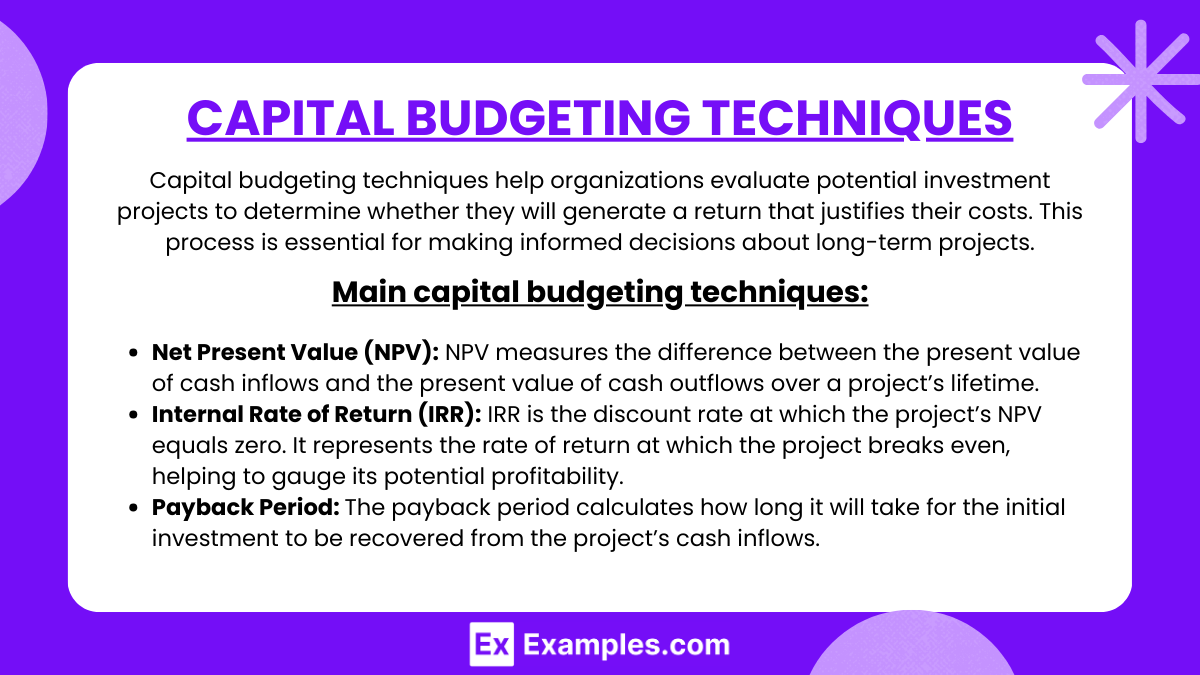

Capital Budgeting Techniques

Capital budgeting techniques help organizations evaluate potential investment projects to determine whether they will generate a return that justifies their costs. This process is essential for making informed decisions about long-term projects, such as purchasing equipment, launching new products, or expanding operations. Here are the main capital budgeting techniques and what they assess:

1. Net Present Value (NPV)

NPV measures the difference between the present value of cash inflows and the present value of cash outflows over a project’s lifetime. It helps determine whether a project is likely to be profitable.

How It Works:

- A positive NPV means that the project’s expected returns exceed the cost, making it a viable investment.

- A negative NPV suggests the project’s costs outweigh its benefits, indicating it should be rejected.

Strengths: Considers the time value of money and provides a direct measure of how much value a project adds.

Example: If a project’s NPV is $200,000, it’s expected to add that amount to the company’s value, assuming all projections hold true.

2. Internal Rate of Return (IRR)

IRR is the discount rate at which the project’s NPV equals zero. It represents the rate of return at which the project breaks even, helping to gauge its potential profitability.

How It Works:

- If the IRR is greater than the required rate of return or cost of capital, the project is considered acceptable.

- A lower IRR than the required return suggests the project should be rejected.

Strengths: Provides a percentage return, making it easy to compare with the company’s hurdle rate or other investment options.

Example: A project with an IRR of 15% would be considered attractive if the company’s required return is 10%.

3. Payback Period

The payback period calculates how long it will take for the initial investment to be recovered from the project’s cash inflows.

How It Works:

- Projects with shorter payback periods are generally more desirable, especially when liquidity is a concern.

- However, this technique ignores the time value of money and cash flows beyond the payback period.

Strengths: Simple to understand and provides a quick measure of liquidity risk.

Example: If an investment of $100,000 is expected to generate $25,000 annually, the payback period is four years.

Analyzing Impact on Financial Health and Strategic Goals

Evaluating the impact of financial decisions on an organization’s financial health and strategic goals is essential to ensure that the business remains sustainable and aligned with its long-term vision. Here’s a guide to understanding the primary areas to consider when assessing how decisions affect financial health and strategic objectives:

1. Impact on Profitability

Profitability is a key indicator of financial health and affects an organization’s ability to reinvest in growth, distribute dividends, or pay down debt.

- Gross and Net Profit Margins: Affects the organization’s ability to generate income from sales, impacting operational efficiency.

- Return on Assets (ROA): Measures how effectively the company uses its assets to generate profit. Higher profitability enhances a company’s ability to fund new projects that support strategic goals.

Strategic Impact: A profitable company can allocate more resources toward growth initiatives, innovation, and achieving long-term goals. Low profitability, however, can limit opportunities for reinvestment and may force the company to reassess priorities.

2. Cash Flow and Liquidity Management

Cash flow is critical for day-to-day operations and long-term stability. Good cash flow management supports both operational needs and strategic initiatives.

- Operating Cash Flow: Strong cash flow from operations indicates the company can cover its expenses without needing external funding, freeing up funds for strategic projects.

- Liquidity Ratios: Ratios like the current ratio and quick ratio reveal the company’s ability to meet short-term obligations. Sufficient liquidity ensures financial stability and flexibility.

Strategic Impact: Positive cash flow and high liquidity improve a company’s ability to respond to strategic opportunities and unforeseen challenges. Inadequate cash flow or liquidity constraints may hinder project funding, slowing progress toward strategic goals.

3. Leverage and Capital Structure

The way a company finances its operations, through debt or equity, influences its risk level and flexibility in pursuing growth.

- Debt-to-Equity Ratio: A balanced approach to debt and equity helps the company maintain financial flexibility. High debt levels, however, may restrict future borrowing for strategic projects.

- Interest Coverage Ratio: Indicates the company’s ability to cover interest expenses, crucial for financial stability and creditworthiness.

Strategic Impact: A well-structured capital mix provides stability, reducing risk while supporting strategic investments. High leverage can limit strategic choices and force the company to prioritize debt repayment over growth.

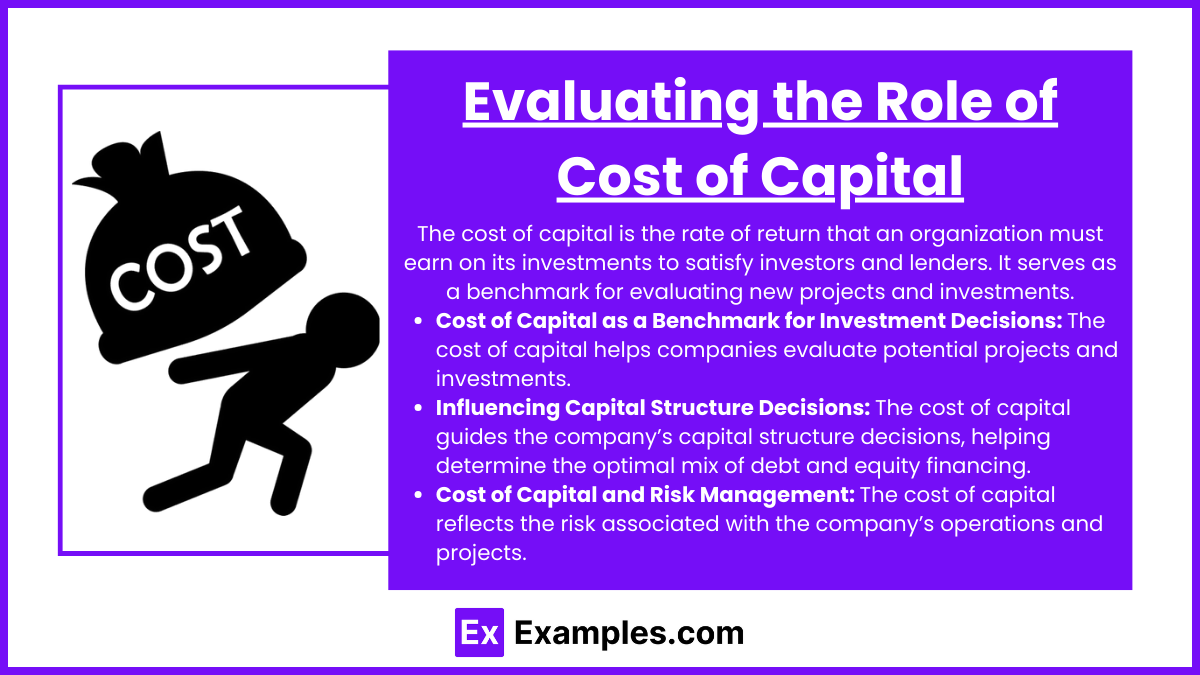

Evaluating the Role of Cost of Capital

The cost of capital is the rate of return that an organization must earn on its investments to satisfy investors and lenders. It serves as a benchmark for evaluating new projects and investments, guiding financial decisions to ensure that returns meet or exceed investor expectations. Understanding the role of cost of capital is critical for making informed strategic and financial decisions.

1. Cost of Capital as a Benchmark for Investment Decisions

The cost of capital helps companies evaluate potential projects and investments by providing a minimum acceptable return threshold.

- Investment Evaluation: For a project to be viable, its expected return must exceed the company’s cost of capital. If the return on a project is lower than the cost of capital, it may reduce shareholder value and should typically be avoided.

- Net Present Value (NPV) and Internal Rate of Return (IRR): The cost of capital serves as the discount rate in NPV calculations and the comparison rate for IRR. A positive NPV or an IRR greater than the cost of capital indicates a value-adding project.

Example: If a company has a cost of capital of 8% and a project offers a 12% return, the project would be accepted as it exceeds the cost of capital.

2. Influencing Capital Structure Decisions

The cost of capital guides the company’s capital structure decisions, helping determine the optimal mix of debt and equity financing.

- Debt vs. Equity Financing: Debt generally has a lower cost than equity due to tax-deductible interest expenses. However, excessive debt increases financial risk, which can ultimately raise the cost of capital.

- Optimal Capital Structure: Companies aim to balance debt and equity to minimize the overall cost of capital, ensuring a lower hurdle rate for investments and improving returns for shareholders.

Example: A firm with a high equity cost may choose to add more debt to its capital structure, as long as it doesn’t significantly increase risk.

3. Cost of Capital and Risk Management

The cost of capital reflects the risk associated with the company’s operations and projects. Higher risk levels lead to a higher cost of capital, impacting project selection and financial strategy.

- Risk Premium: Investors require higher returns for higher risk, meaning riskier companies have a higher cost of equity. Managing risk effectively can help lower the cost of capital.

- Project Risk Assessment: Projects with higher risk should be expected to earn higher returns to justify the added risk. If a project increases the company’s overall risk profile, it may also raise the cost of capital.

Example: A technology startup with high market risk may have a higher cost of capital than an established utility company, influencing the types of projects it undertakes.

Examples

Example 1: Real Estate Investment

An individual decides to invest in residential real estate by purchasing a rental property. This investment decision involves evaluating the property’s location, potential rental income, market trends, and associated costs (such as maintenance and taxes). The investor assesses the long-term appreciation potential of the property and the cash flow generated from rent, weighing the benefits against the risks of property management and market fluctuations.

Example 2: Stock Market Investment

An investor chooses to buy shares of a technology company after analyzing its financial health, growth potential, and industry trends. This decision involves researching the company’s earnings reports, market position, and competitive advantages. The investor also considers their risk tolerance and investment horizon, deciding whether to invest for short-term gains or long-term growth, thus reflecting a strategy based on personal financial goals.

Example 3: Bond Investment

A conservative investor opts to purchase government bonds as part of a fixed-income strategy. This decision is made to secure a steady income stream with lower risk compared to stocks. The investor assesses the bond’s interest rate, maturity, and the issuing government’s creditworthiness. By investing in bonds, the investor aims to preserve capital while earning interest, balancing their portfolio to mitigate volatility.

Example 4: Mutual Funds vs. Individual Stocks

An individual is considering whether to invest in a mutual fund or directly purchase individual stocks. This investment decision requires evaluating factors such as diversification, management fees, and the investor’s own expertise in selecting stocks. If the individual prefers a hands-off approach and diversification, they may choose a mutual fund, while a more experienced investor seeking higher potential returns may opt for direct stock investments.

Example 5: Retirement Accounts

A young professional decides to contribute to a retirement account, such as a 401(k) or an IRA. This investment decision involves evaluating contribution limits, tax advantages, and investment options within the account. The individual considers their retirement goals and time horizon, deciding how much to invest regularly and which funds or assets to allocate within the retirement account to achieve growth over time. This strategic decision is critical for long-term financial security.

Practice Questions

Question 1

Which of the following factors is most important when evaluating an investment opportunity?

A) The potential for short-term profits

B) The alignment with an investor’s financial goals and risk tolerance

C) The opinions of friends and family

D) The popularity of the investment in social media

Correct Answer: B) The alignment with an investor’s financial goals and risk tolerance.

Explanation: When making investment decisions, it is crucial to consider how well an investment aligns with an investor’s long-term financial goals and risk tolerance. This assessment helps ensure that the investment is suitable for the individual’s financial situation and objectives, leading to better decision-making. Options A, C, and D may influence decisions but should not take precedence over personal financial goals and risk assessment.

Question 2

What is a common reason investors diversify their portfolios?

A) To maximize short-term returns

B) To reduce overall investment risk

C) To ensure all investments are in high-growth sectors

D) To avoid all market fluctuations

Correct Answer: B) To reduce overall investment risk.

Explanation: Diversification involves spreading investments across different asset classes, sectors, or geographic regions to minimize risk. By not putting all capital into a single investment or type of investment, investors can protect themselves from significant losses if one asset underperforms. While options A and C focus on returns and specific sectors, diversification’s primary purpose is risk reduction. Option D is misleading, as it is impossible to avoid all market fluctuations entirely.

Question 3

Which investment strategy focuses on buying securities that appear undervalued?

A) Growth investing

B) Value investing

C) Income investing

D) Momentum investing

Correct Answer: B) Value investing.

Explanation: Value investing is a strategy that involves identifying and purchasing securities that are believed to be undervalued relative to their intrinsic value. Investors using this strategy look for stocks that are trading for less than their perceived worth, based on fundamental analysis. Growth investing, in contrast, focuses on companies expected to grow at an above-average rate, while income investing prioritizes generating regular income from dividends. Momentum investing relies on trends in price movement rather than intrinsic value assessments.