In the vast landscape of economic theory, perfect competition stands as a fundamental concept that shapes our understanding of markets, competition, and pricing mechanisms. This article delves into the realm of perfect competition, offering insights into its definition, characteristics, and real-world examples. Whether you’re a student seeking to grasp the basics or an enthusiast eager to explore economic intricacies, this article provides a comprehensive guide to perfect competition.

Table of Contents

- 1. Simple Perfect Competition Example

- 2. The Firm and the Industry under Perfect Competition

- 3. Sample Perfect Competition Example

- 4. Perfect Competition Questions

- 5. Perfect Competition Monopoly

- 6. Basic Perfect Competition Example

- 7. Draft Perfect Competition Example

- 8. Perfect Competition and Other Market Structures

- 9. Highly Competitive Markets Example

- 10. Perfect Competition and Welfare

- 11. Perfect Competition in Markets with Adverse Selection

- 12. Editable Perfect Competition Example

- 13. Perfect Competition and Monopoly

- 14. Perfect Competition, Oligopoly and Monopolies

- 15. Note on the History of Perfect Competition

- 16. Printable Perfect Competition Example

- 17. Monopoly and Perfect Competition Compared

- 18. Perfect Competition Model of Markets

- 19. Producer Theory Perfect Competition

- 20. Standard Perfect Competition Example

- 21. The Perfectly Competitive Market

- 22. Price Determination Under Perfect Competition

- 23. Modern Perfect Competition Example

- 24. Creative Perfect Competition Example

- 25. Perfect Competition and Economic Welfare

- 26. Basic Perfect Competition and Monopoly

- 27. Perfect Competition and Profit Maximization

- 28. Perfectly Competitive Markets Example

- 29. Layout Perfect Competition Example

- 30. Outline Perfect Competition Example

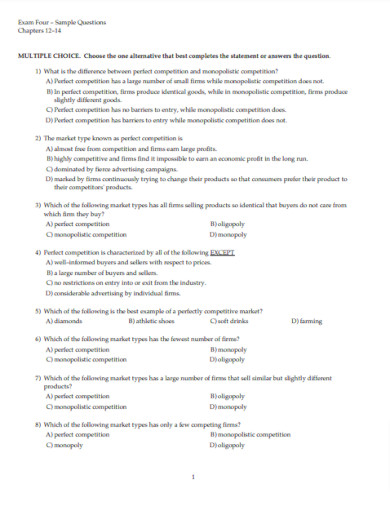

- 31. Perfect Competition Multiple Choice Questions

- 32. Perfect Competition Market Structure

- What is Perfect Competition?

- How to Understand Perfect Competition?

- Step 1: Grasping the Basic Elements

- Step 2: Observing Cause and Effect

- Step 3: Exploring Positive Feedback Loop

- Step 4: Analyzing Long-Term Goals

- FAQs

- What is the primary goal of participants in a perfectly competitive market?

- Is perfect competition a realistic market scenario?

- How does perfect competition relate to the concept of correlation?

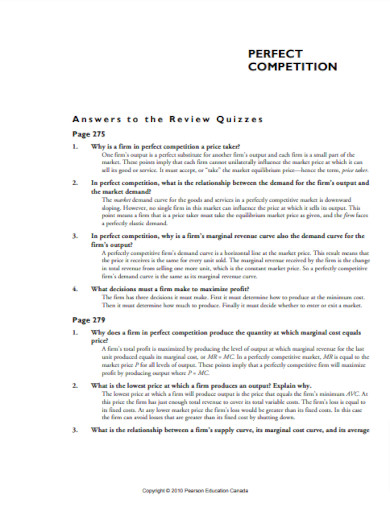

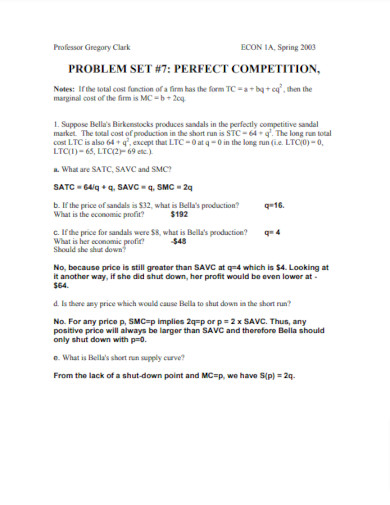

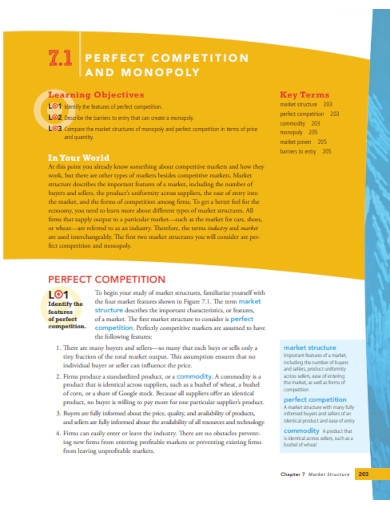

1. Simple Perfect Competition Example

sfu.ca

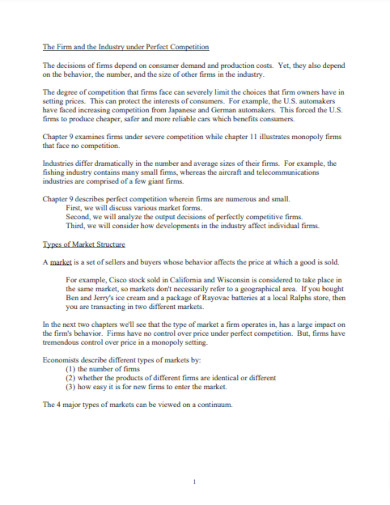

2. The Firm and the Industry under Perfect Competition

csun.edu

3. Sample Perfect Competition Example

unf.edu

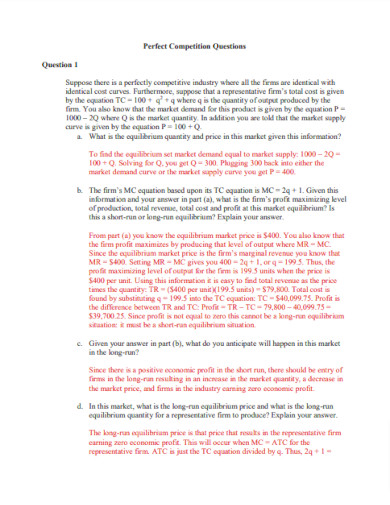

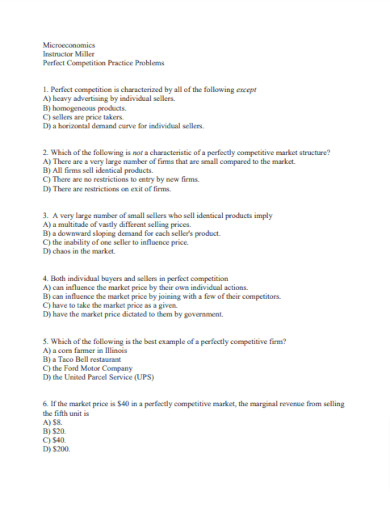

4. Perfect Competition Questions

users.ssc.wisc.edu

5. Perfect Competition Monopoly

sites.bu.edu

6. Basic Perfect Competition Example

faculty.econ.ucdavis.edu

7. Draft Perfect Competition Example

uir.unisa.ac.za

8. Perfect Competition and Other Market Structures

account.ache.org

9. Highly Competitive Markets Example

manhassetschools.org

10. Perfect Competition and Welfare

econ.ucla.edu

11. Perfect Competition in Markets with Adverse Selection

bfi.uchicago.edu

12. Editable Perfect Competition Example

fimt-ggsipu.org

13. Perfect Competition and Monopoly

dsfepf2015.weebly.com

14. Perfect Competition, Oligopoly and Monopolies

globalyouth.wharton.upenn.edu

15. Note on the History of Perfect Competition

economia.unam.mx

16. Printable Perfect Competition Example

myweb.dmacc.edu

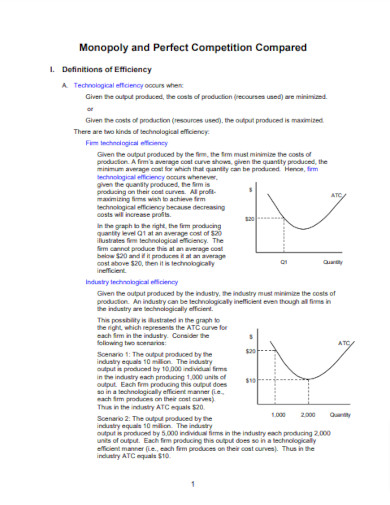

17. Monopoly and Perfect Competition Compared

courses.missouristate.edu

18. Perfect Competition Model of Markets

web.mst.edu

19. Producer Theory Perfect Competition

columbia.edu

20. Standard Perfect Competition Example

mlcompton.files.wordpress.com

21. The Perfectly Competitive Market

cambridgescholars.com

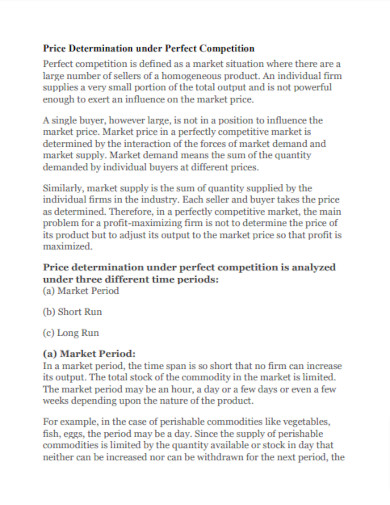

22. Price Determination Under Perfect Competition

soghracollege.com

23. Modern Perfect Competition Example

core.ac.uk

24. Creative Perfect Competition Example

magadhmahilacollege.org

25. Perfect Competition and Economic Welfare

dcpopp.expressions.syr.edu

26. Basic Perfect Competition and Monopoly

users.ox.ac.uk

27. Perfect Competition and Profit Maximization

bpb-us-e1.wpmucdn.com

28. Perfectly Competitive Markets Example

belkcollegeofbusiness.charlotte.edu

29. Layout Perfect Competition Example

egyankosh.ac.in

30. Outline Perfect Competition Example

um.es

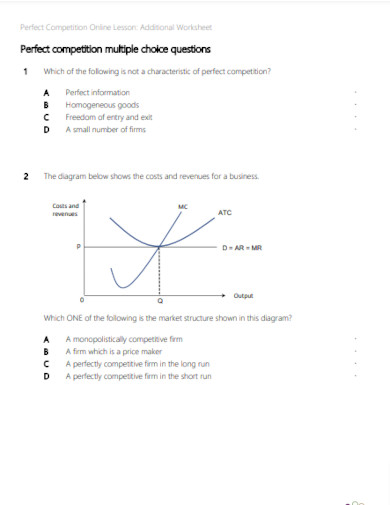

31. Perfect Competition Multiple Choice Questions

32. Perfect Competition Market Structure

thebusinessguys.ie

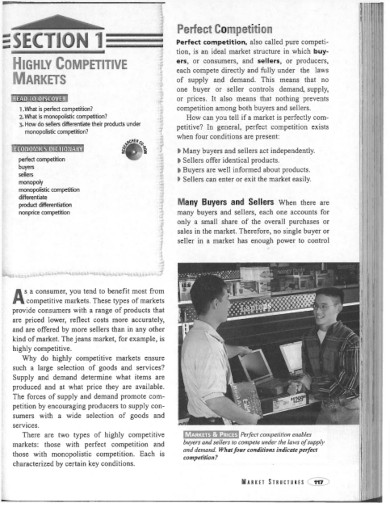

What is Perfect Competition?

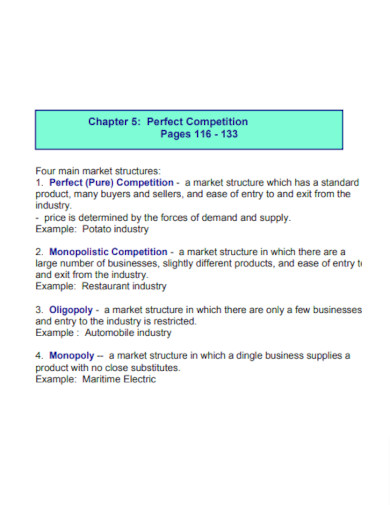

Perfect competition, within the context of microeconomics, is a theoretical market structure that serves as a foundation for understanding how markets operate under specific conditions. In a perfectly competitive market, numerous buyers and sellers engage in transactions involving identical products. Each participant is a price taker, implying they have no influence on the market price. This context offers a simplified yet insightful way to study market dynamics and their impact on prices and output levels.

How to Understand Perfect Competition?

To gain a holistic understanding of perfect competition, follow this step-by-step guide. Each step sheds light on different aspects of this economic concept, allowing you to grasp its nuances effectively.

Step 1: Grasping the Basic Elements

Begin by understanding the foundational elements of perfect competition. These include a large number of buyers and sellers, homogeneous products, ease of market entry and exit, perfect information availability, and price-taking behavior. These factors collectively create an environment where no single entity can influence the market economy.

Step 2: Observing Cause and Effect

Delve into the cause-and-effect dynamics within a perfectly competitive market. The interaction between supply and demand leads to equilibrium, determining the market-clearing price and quantity. This observation highlights the interplay between buyer and seller decisions and how they impact market outcomes.

Step 3: Exploring Positive Feedback Loop

Explore the concept of positive feedback within perfect competition. As prices rise, more suppliers are incentivized to enter the market, increasing supply and potentially leading to price decreases. Conversely, lower prices may drive some suppliers to exit, potentially causing prices to rise. This positive feedback loop maintains equilibrium.

Step 4: Analyzing Long-Term Goals

Examine the long-term goals of participants in a perfectly competitive market. Since products are homogenous, buyers often choose the lowest-priced option. For sellers, the objective is to maximize profit, driving efficiency and innovation to remain competitive.

FAQs

What is the primary goal of participants in a perfectly competitive market?

In a perfectly competitive market, both buyers and sellers seek to optimize their positions. Buyers aim to acquire goods at the lowest price, while sellers strive to maximize their profits by offering goods efficiently.

Is perfect competition a realistic market scenario?

While perfect competition serves as a theoretical model, real-world markets often deviate from its assumptions. Imperfect information, product differentiation, and other factors can lead to market structures that differ from perfect competition.

How does perfect competition relate to the concept of correlation?

Perfect competition focuses on the relationship between price and quantity supplied/demanded. Correlation, on the other hand, refers to the statistical association between two variables. While not directly linked, both concepts involve understanding relationships within data.

In conclusion, understanding perfect competition is crucial for comprehending the intricate dance of supply and demand within markets. By grasping the essential elements, observing cause-and-effect relationships, exploring feedback loops, and analyzing long-term goals, you can unlock insights into how this model shapes economic landscapes. While perfect competition may be an idealized scenario, it remains a cornerstone of economic thought, providing valuable insights into the broader world of commerce and trade.