A monopoly exists when a single firm dominates a market with no close substitutes, controlling supply and prices. Unlike perfect competition, where many firms sell identical products and no single firm can influence prices, a monopoly restricts output to maximize profits. This market structure leads to higher prices and less consumer choice. Monopolies often result from barriers to entry, such as patents, resource control, or government regulations, creating an environment starkly different from perfect competition.

What is Monopoly?

A monopoly is a market structure where a single firm exclusively controls the entire supply of a product or service, faces no competition, and can set prices. This leads to restricted output, higher prices, and less consumer choice compared to competitive markets.

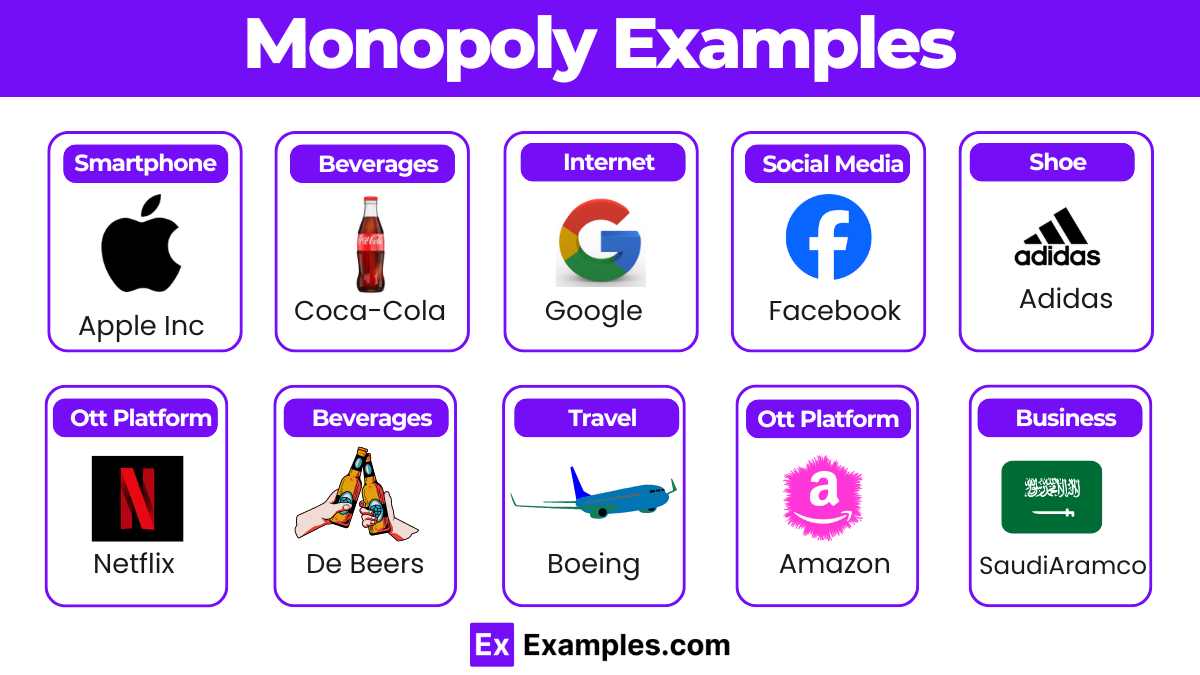

Monopoly Examples

- Microsoft – Dominates the operating system market with Windows, limiting competition and controlling software distribution.

- Google – Leads the search engine market, significantly influencing online advertising and data collection.

- Amazon – Controls a substantial share of online retail, affecting pricing and market entry for competitors.

- Facebook – Dominates social media, impacting advertising and user data control across platforms.

- Apple – Has a stronghold on the smartphone market, particularly with iOS devices and the App Store.

- Netflix – Leading streaming service, influences pricing and content availability in the entertainment industry.

- AT&T – Major player in telecommunications, affecting pricing and service availability for consumers.

- Intel – Dominates the microprocessor market, controlling supply for computers and other devices.

- Boeing – Leading aircraft manufacturer, influencing pricing and availability in the aviation industry.

- De Beers – Controls the diamond market, significantly affecting prices and supply.

- Pfizer – Major pharmaceutical company, influences drug prices and availability.

- Coca-Cola – Dominates the soft drink market, impacting pricing and competition.

- Visa – Leading payment processing company, affecting transaction fees and service availability.

- Monsanto – Controls a significant portion of the agricultural seed market, influencing prices and farming practices.

- Comcast – Major player in cable television and internet services, impacting pricing and service options.

- Luxottica – Dominates eyewear, owning several brands and retail outlets, affecting prices and availability.

- ESPN – Leading sports network, significantly influencing sports broadcasting and advertising.

- Amtrak – Sole provider of intercity passenger rail service in the U.S., affecting travel options and pricing.

- Railtrack – Controls UK’s railway infrastructure, impacting service quality and pricing.

- Gazprom – Major natural gas supplier, influencing energy prices and availability in Europe.

- Saudi Aramco – Dominates the oil market, affecting global oil prices and supply.

- USPS – Sole provider of certain postal services in the U.S., impacting pricing and service options.

- T-Mobile – Major wireless carrier, influencing pricing and competition in the telecommunications market.

- Alibaba – Dominates e-commerce in China, affecting pricing and market entry for competitors.

- Johnson & Johnson – Major player in healthcare products, influencing prices and availability.

- Disney – Dominates entertainment, particularly in movies and theme parks, impacting content and pricing.

Monopoly Types

- Natural Monopoly – Dominance due to high infrastructure costs, making it inefficient for new competitors to enter the market.

- Government Monopoly – Monopoly established and maintained by the government to control specific sectors or industries for public interest.

- Technological Monopoly – Dominance achieved through unique technology or innovation that competitors cannot easily replicate.

- Geographic Monopoly – Monopoly resulting from a company’s control over a specific geographic area’s resources or market.

- Legal Monopoly – Exclusive rights granted by law to a company, preventing others from entering the market.

- Virtual Monopoly – Control over digital platforms or online services where competition is minimal or nonexistent.

- Resource Monopoly – Monopoly created by a company’s control over essential natural or raw resources required by an industry.

- Utility Monopoly – Dominance in public utilities like water, electricity, or gas, often regulated by the government.

- State Monopoly – Monopoly operated by the state, often in industries deemed essential for national security or welfare.

- Price-Discriminating Monopoly – Monopoly that charges different prices to different consumer groups for the same product or service.

Features of Monopoly

- Single Seller – One firm controls the entire market, acting as the sole producer and seller of a product or service.

- No Close Substitutes – The product offered by the monopoly has no close substitutes, making it unique in the market.

- Price Maker – The monopoly firm has significant control over the price, setting it to maximize profits without direct competition.

- High Barriers to Entry – Significant obstacles prevent new firms from entering the market, such as high costs, legal restrictions, or technological advantages.

- Economies of Scale – The monopoly firm benefits from economies of scale, reducing per-unit costs as production increases.

- Consumer Dependency – Consumers rely on the monopoly firm for the product, with limited or no alternative sources available.

- Lack of Competition – Absence of competition leads to less innovation and potentially lower-quality products or services.

- Profit Maximization – The monopoly aims to maximize profits by setting prices higher than in competitive markets.

- Regulation and Oversight – Monopolies may be subject to government regulation to prevent abuse of market power and protect consumer interests.

- Market Influence – The monopoly has significant influence over market trends, prices, and overall economic conditions within the industry.

Monopoly in Economics

A monopoly in economics refers to a market structure where a single firm dominates the entire market with no close substitutes, allowing it to control prices and output. In a market economy, monopolies can arise due to barriers to entry, such as patents, resource control, or government regulations. Unlike a perfectly competitive market, where many firms compete and prices are determined by supply and demand, a monopoly restricts output to maximize profits, leading to higher prices and reduced consumer choice. Monopolies can impact a market economy by limiting competition, reducing efficiency, and potentially leading to market failure.

Monopoly Rules

- Market Control: A single firm must dominate the market with no significant competition.

- Barriers to Entry: High entry barriers such as patents or resource control prevent new competitors from entering.

- Price Setting: The monopolist has the power to set prices due to lack of competition.

- Vendor Application: In Vendor Application Vendors must often apply for permission to operate within the monopolist’s market, limiting competition.

- Regulatory Compliance: Monopolies must comply with regulations to prevent abuse of market power.

- Consumer Impact: Monopolies can lead to higher prices and limited choices for consumers.

Monopoly Regulations

- Antitrust Laws: Enforced to prevent monopolistic practices and promote fair competition.

- Price Controls: Regulations may impose limits on prices to protect consumers from exploitation.

- Market Entry Facilitation: Policies to lower barriers for new firms entering the market.

- Consumer Protection: Ensures that consumers are not negatively impacted by monopolistic practices.

- Vendor Application Oversight: Monitoring vendor applications to prevent unfair market dominance by a single firm.

- Public Awareness: Educating the public about monopolies, including how misconceptions like the Mandela Effect can distort understanding of market regulations.

Antitrust Regulations in Action

- Breaking Up Monopolies: Governments can dismantle companies that dominate a market to restore competition, influencing their business marketing plan.

- Preventing Mergers: Authorities block or scrutinize mergers that could lead to reduced competition.

- Price Fixing Penalties: Firms colluding to set prices face severe fines and legal actions.

- Promoting Fair Trade: Regulations ensure small businesses can compete fairly, impacting their business marketing plans.

- Monitoring Market Practices: Regular surveillance prevents anti-competitive practices.

- Consumer Protection: Laws safeguard consumers from monopolistic exploitation, ensuring fair market access.

How Do Antitrust Laws Protect Consumers?

- Preventing Monopolies: Antitrust laws stop single firms from dominating markets, ensuring fair competition unlike in a command economy.

- Encouraging Lower Prices: By fostering competition, antitrust laws drive down prices for consumers.

- Ensuring Quality: Competition incentivizes companies to improve product quality and innovation.

- Blocking Price Fixing: Laws prevent companies from colluding to set high prices, protecting consumer interests.

- Promoting Choice: Consumers have access to a variety of products and services due to diverse market players.

- Preventing Abuse: Antitrust laws curb unfair practices that exploit consumers, ensuring a fair market environment.

- Facilitating Market Entry: Antitrust regulations lower barriers for new firms, increasing competition and choices for consumers.

- Enhancing Innovation: By preventing monopolies, these laws encourage continuous innovation, benefiting consumers with better and more advanced products.

Pros and Cons of a Monopoly

| Aspect | Pros | Cons |

|---|---|---|

| Market Control | Can streamline operations and reduce duplication of efforts. | Leads to lack of competition, reducing consumer choice. |

| Pricing Power | Allows for price stability and long-term planning. | Results in higher prices for consumers due to lack of competition. |

| Innovation | Potential for significant investment in research and development. | May lead to complacency and reduced innovation over time. |

| Economies of Scale | Large scale production can lower costs, potentially reducing prices. | Savings may not be passed on to consumers, leading to higher profits only for the monopolist. |

| Efficiency | Can achieve high levels of efficiency due to control over the market. | Efficiency gains are often not shared with consumers or the broader market. |

| Customer Service | Consistent customer service experience due to centralized control. | Lack of competition can lead to poor customer service. |

| Barriers to Entry | High barriers can protect the company from new entrants, ensuring stability. | High barriers prevent new companies from entering, stifling competition and innovation. |

Monopolies form due to high barriers to entry, such as patents, resource control, or government regulations.

Advantages include potential for economies of scale, price stability, and significant investment in research and development.

Disadvantages include higher prices, reduced consumer choice, and potential for inefficiency and lack of innovation.

Monopolies can set higher prices since they face no competition.

Yes, monopolies can lead to market failure by reducing competition and efficiency.

Governments use antitrust laws and regulations to prevent and break up monopolies.

Price discrimination is when a monopolist charges different prices to different consumers for the same product.

Monopolies can lead to higher prices, less choice, and potentially lower quality of goods and services.

Patents grant exclusive rights to produce a product, creating a temporary monopoly.

In a monopoly, one firm controls the market, while in perfect competition, many firms compete with identical products.