Equity Valuation: Applications and Processes

Equity Valuation: Applications and Processes” is a fundamental topic for finance professionals and CFA candidates, focusing on methods to assess the intrinsic value of equity investments. Through approaches such as Discounted Cash Flow (DCF), Dividend Discount Model (DDM), and relative valuation, analysts can determine a stock’s fair value, guiding investment decisions in scenarios like mergers, acquisitions, IPOs, and portfolio management. This topic emphasizes understanding key inputs—like discount rates and growth projections—and applying valuation models to optimize portfolio returns, balance risk, and make informed investment recommendations.

Learning Objectives

In studying “Equity Valuation: Applications and Processes” for the CFA Exam, you should learn to apply various valuation techniques to assess the intrinsic value of equity investments, including Discounted Cash Flow (DCF) analysis, Dividend Discount Model (DDM), and relative valuation methods. Evaluate how these approaches assist in determining the fair value of stocks for different market scenarios, such as mergers, acquisitions, IPOs, and portfolio management. Analyze the principles behind key valuation inputs like discount rates, growth rates, and cash flow projections. Additionally, explore how these models inform asset allocation and investment decisions, and practice interpreting valuation results in CFA-level case studies.

1. Understanding the Role of Equity Valuation

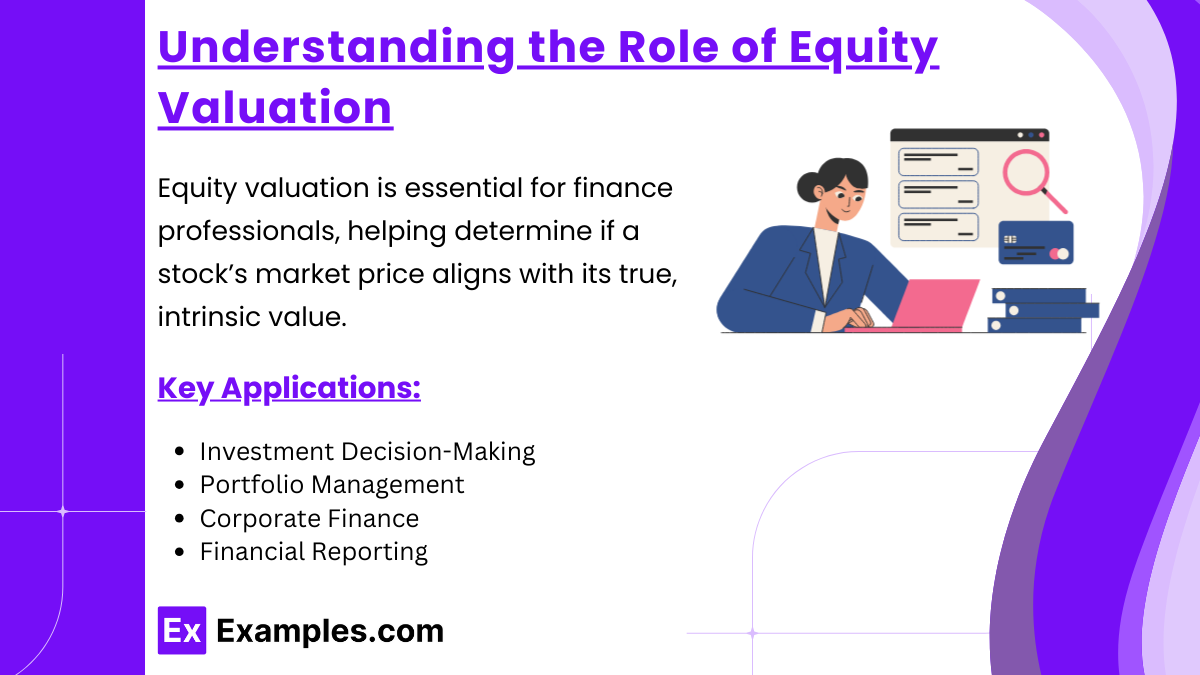

Equity valuation is a fundamental skill for finance professionals, playing a pivotal role in investment analysis and decision-making. By determining the intrinsic value of a stock, equity valuation helps in understanding whether the current market price reflects the true worth of the company or if it is overvalued or undervalued.

Key Applications of Equity Valuation :

- Investment Decision-Making: By estimating intrinsic value, investors can identify undervalued stocks to buy or overvalued stocks to avoid or sell, ultimately aiming to make decisions that optimize returns.

- Portfolio Management: For portfolio managers, equity valuation is critical in constructing and rebalancing portfolios. It helps in selecting a balanced mix of assets, which can enhance portfolio performance and manage risk over time.

- Corporate Finance: Equity valuation assists company leaders in making informed decisions related to mergers and acquisitions, share buybacks, and capital budgeting. Knowing a company’s true worth enables management to allocate resources effectively and make strategic choices for growth.

- Financial Reporting: Accurate equity valuation is necessary for transparent financial reporting, helping companies assess asset values and comply with regulations, which supports investor confidence and market stability.

Why Intrinsic Value Matters

The intrinsic value of a stock represents its “true” worth, based on the company’s expected performance and potential to generate future cash flows. Unlike the market price, which fluctuates with investor sentiment and market dynamics, intrinsic value focuses on the company’s fundamental attributes. Intrinsic valuation methods help investors avoid emotional and speculative influences, enabling rational, data-driven decisions. By comparing the intrinsic value to the current market price, analysts can determine whether a stock is undervalued—presenting a potential investment opportunity—or overvalued, suggesting it may be best avoided or sold.

2. Equity Valuation Approaches

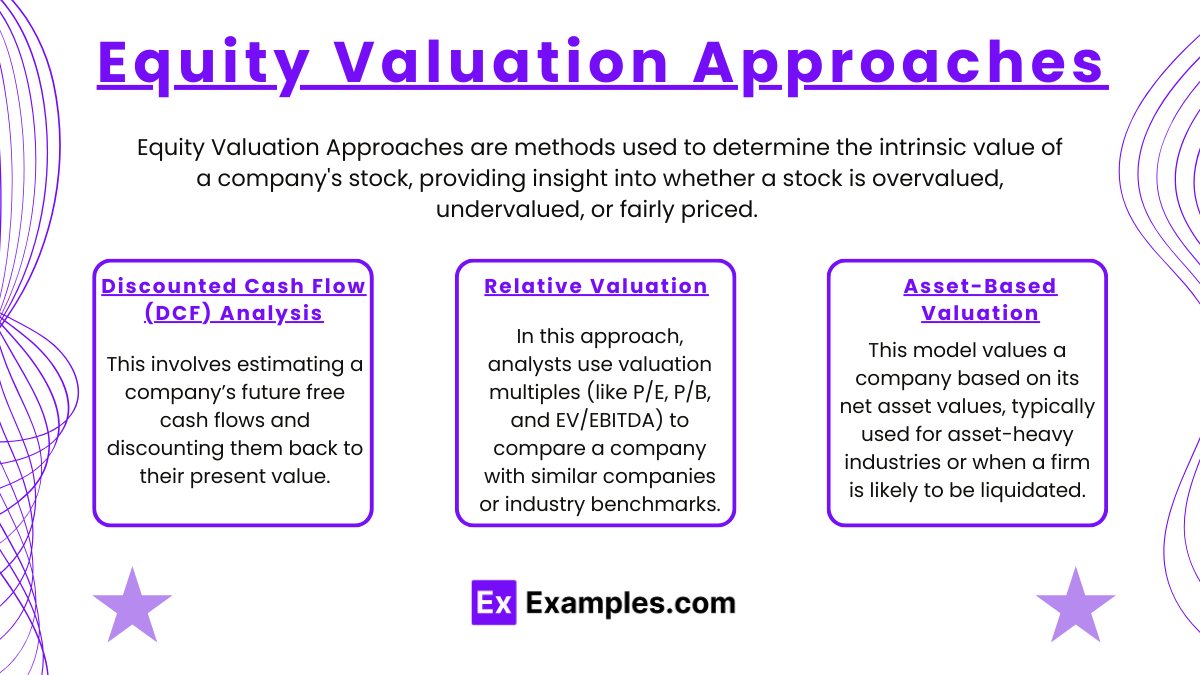

Equity Valuation Approaches are methods used to determine the intrinsic value of a company’s stock, providing insight into whether a stock is overvalued, undervalued, or fairly priced. These approaches include

- Discounted Cash Flow (DCF) Analysis: This involves estimating a company’s future free cash flows and discounting them back to their present value. Key steps include forecasting revenues, expenses, and capital expenditures, then selecting an appropriate discount rate (often derived from the weighted average cost of capital).

- Dividend Discount Model (DDM): Primarily used for companies with consistent dividend payouts, this model calculates intrinsic value based on future dividends discounted at the required rate of return.

- Free Cash Flow to Equity (FCFE): For companies without steady dividends, FCFE discounts the company’s free cash flows to equity holders.

- Relative Valuation: In this approach, analysts use valuation multiples (like P/E, P/B, and EV/EBITDA) to compare a company with similar companies or industry benchmarks. It’s simpler than DCF but is sensitive to market conditions and industry norms.

- Asset-Based Valuation: This model values a company based on its net asset values, typically used for asset-heavy industries or when a firm is likely to be liquidated.

3. Processes in Equity Valuation

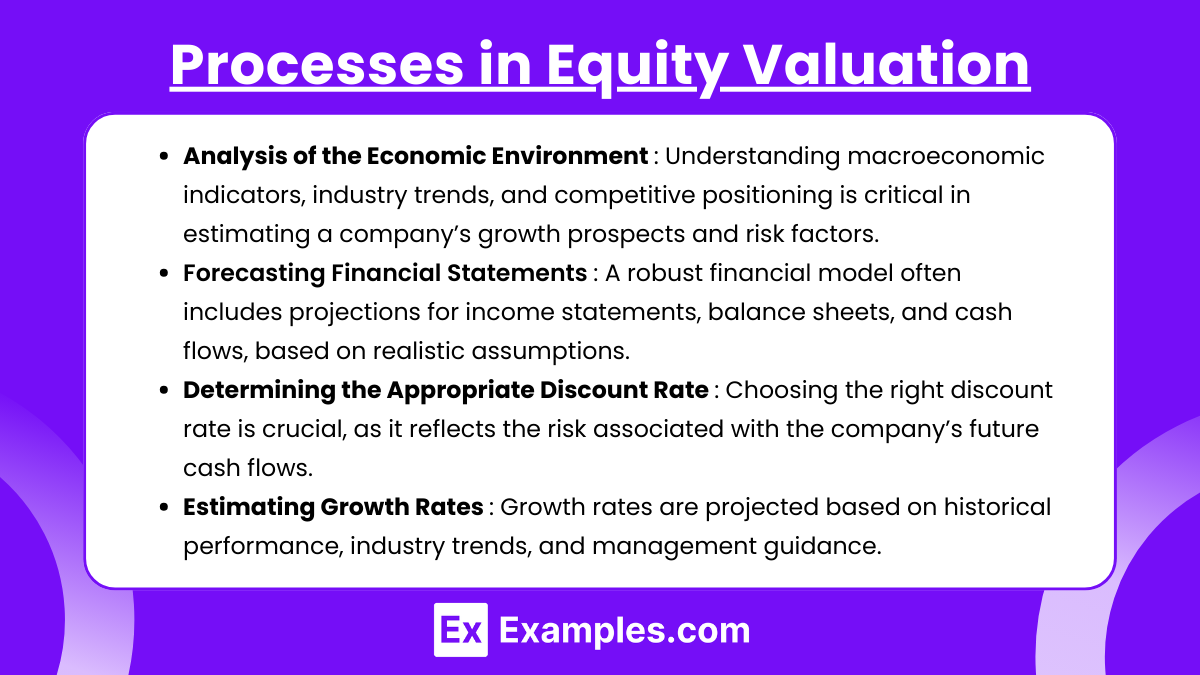

- Analysis of the Economic Environment: Understanding macroeconomic indicators, industry trends, and competitive positioning is critical in estimating a company’s growth prospects and risk factors.

- Forecasting Financial Statements: A robust financial model often includes projections for income statements, balance sheets, and cash flows, based on realistic assumptions.

- Determining the Appropriate Discount Rate: Choosing the right discount rate is crucial, as it reflects the risk associated with the company’s future cash flows. Analysts often use the Capital Asset Pricing Model (CAPM) to estimate the required return on equity.

- Estimating Growth Rates: Growth rates are projected based on historical performance, industry trends, and management guidance. They play a significant role in models like the DDM and FCFE.

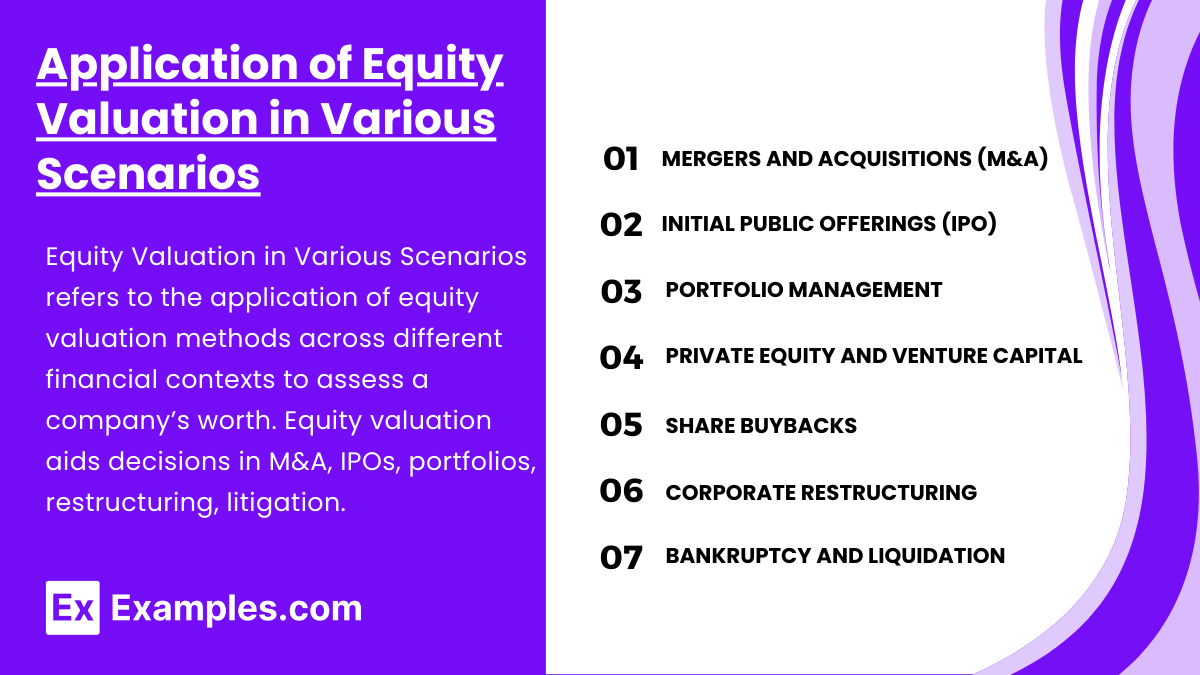

4. Application of Equity Valuation in Various Scenarios

Equity Valuation in Various Scenarios refers to the application of equity valuation methods across different financial contexts to assess a company’s worth. By estimating a stock’s intrinsic value, equity valuation helps investors and analysts make informed decisions based on specific scenarios, such as mergers and acquisitions (M&A), initial public offerings (IPOs), portfolio management, corporate restructuring, and litigation.

- Mergers and Acquisitions (M&A): Valuation models support fair value assessments of target companies, ensuring the acquirer does not overpay.

- Initial Public Offerings (IPO): Analysts use valuation methods to set an appropriate price range for newly public companies.

- Portfolio Management: Valuation helps determine asset allocation within portfolios, assisting portfolio managers in balancing undervalued and overvalued stocks to maximize returns.

- Private Equity and Venture Capital: Used to estimate the value of startups and high-growth companies, guiding investment decisions, pricing rounds, and exit strategies.

- Share Buybacks: Companies use valuation to assess whether repurchasing shares is beneficial, often done if management believes shares are undervalued.

- Corporate Restructuring: Valuation aids in deciding asset sales, spin-offs, or divestitures, allowing companies to release value or streamline operations.

- Bankruptcy and Liquidation: Asset-based valuation is often used in these situations to estimate recovery value for creditors and stakeholders.

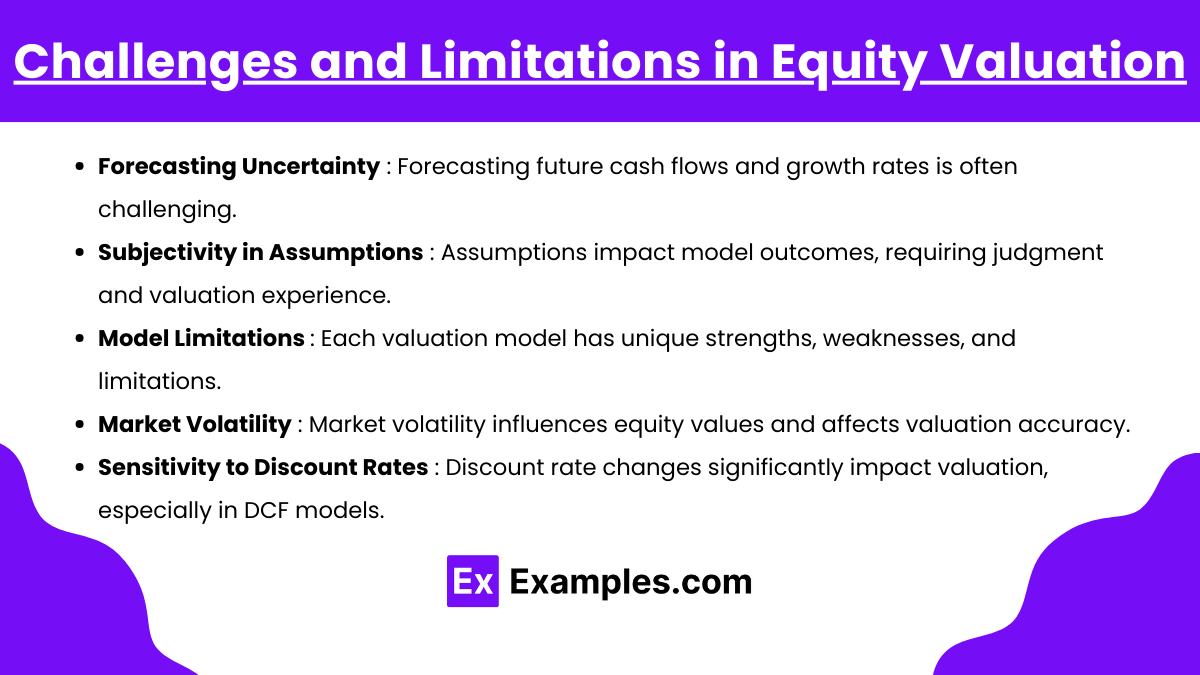

5. Challenges and Limitations in Equity Valuation

- Forecasting Uncertainty: Predicting future cash flows and growth rates accurately can be challenging. Market conditions, regulatory changes, and management decisions may affect future performance.

- Subjectivity in Assumptions: Assumptions like discount rates, growth rates, and financial ratios impact the model’s outcome significantly, requiring sound judgment and experience.

- Model Limitations: Each valuation model has its strengths and weaknesses, and choosing the wrong model or incorrect parameters can lead to inaccurate valuations.

- Market Volatility: Equity values can fluctuate with changes in investor sentiment, economic conditions, or unexpected events, affecting the accuracy of valuations.

- Sensitivity to Discount Rates: Small changes in the discount rate can lead to large swings in valuation, particularly in models like DCF, which makes precise rate selection crucial.

Examples

Example 1: Assessing Target Companies in Mergers and Acquisitions (M&A)

Equity valuation is a critical component in M&A transactions, as it helps acquirers determine a fair purchase price for a target company. For example, a company looking to acquire a competitor would conduct a valuation of the target company’s equity by estimating future cash flows, discounting them to their present value, and comparing this intrinsic value to the target’s market price. This process ensures that the acquirer pays a fair price, ideally identifying undervalued opportunities and avoiding overpayment in transactions.

Example 2: Setting the Price Range for Initial Public Offerings (IPOs)

Before a private company goes public, analysts perform equity valuation to determine an appropriate price range for its shares. For instance, an investment bank assisting in an IPO might use the Discounted Cash Flow (DCF) method to estimate the company’s value based on future earnings. They could also apply multiples from comparable public companies to refine the valuation. This helps establish a fair price for initial shares, balancing the company’s need for capital with investor demand and market conditions.

Example 3: Guiding Investment Decisions in Portfolio Management

Portfolio managers use equity valuation to decide which stocks to buy, hold, or sell. For example, if a stock’s intrinsic value, calculated through methods like DCF or Relative Valuation, is higher than its market price, it may be added to the portfolio as an undervalued investment. By systematically evaluating stocks in this way, portfolio managers can construct diversified portfolios with a mix of undervalued assets, thereby aiming to maximize returns and manage risk effectively.

Example 4: Evaluating Share Buyback Decisions

Companies may conduct share buybacks when they believe their stock is undervalued in the market. For instance, a firm might use Free Cash Flow to Equity (FCFE) valuation to assess its intrinsic value and determine if its stock price is below fair value. If so, the company may initiate a buyback program, repurchasing shares to enhance shareholder value by increasing earnings per share (EPS) and improving the stock’s market price. This application demonstrates the importance of valuation in corporate financial strategy.

Example 5: Estimating Fair Value in Legal Disputes

Equity valuation is frequently used in legal settings, such as shareholder disputes or divorce cases involving significant assets. For example, in a shareholder dispute, a court might require a valuation of a privately held company to determine the fair market value of an ownership stake. Analysts use valuation models, often considering both asset-based and income-based approaches, to arrive at an equitable value. This process provides an objective basis for settlements, ensuring fair outcomes based on the company’s actual worth.

Practice Questions

Question 1

An analyst is valuing a company’s stock using the Dividend Discount Model (DDM). The company is expected to pay a dividend of $2.00 per share next year, and dividends are expected to grow at a constant rate of 4% per year. If the required rate of return for the stock is 8%, what is the intrinsic value of the stock?

A. $25.00

B. $50.00

C. $52.00

D. $40.00

Answer: B. $50.00

Explanation: The Dividend Discount Model (DDM) for a stock with constant growth is given by:

where:

- D1 is the expected dividend next year = $2.00,

- r is the required rate of return = 8% or 0.08,

- g is the dividend growth rate = 4% or 0.04.

Substituting these values:

So, the correct answer is B. $50.00.

This model is used under the assumption of constant dividend growth, and it applies best to companies with stable, predictable dividend patterns, often mature companies.

Question 2

Which of the following statements is a primary challenge when using Discounted Cash Flow (DCF) analysis for equity valuation?

A. DCF analysis ignores the impact of dividends on valuation.

B. DCF analysis requires estimating future cash flows and an appropriate discount rate, both of which involve significant assumptions.

C. DCF analysis can only be used for asset-heavy companies with stable cash flows.

D. DCF analysis is only applicable to companies in cyclical industries.

Answer : B. DCF analysis requires estimating future cash flows and an appropriate discount rate, both of which involve significant assumptions.

Explanation : The primary challenge with DCF analysis is the need to accurately project future cash flows and determine an appropriate discount rate. Both these inputs require substantial assumptions:

- Future cash flows are affected by the company’s projected revenues, expenses, taxes, and changes in working capital, all of which can vary significantly based on market conditions and company performance.

- The discount rate often depends on the company’s cost of capital or required return, which can also fluctuate based on market risk and company-specific factors.

Option A is incorrect because DCF analysis does account for the cash flow generated by the business, which includes dividends indirectly, as dividends are paid out of cash flows.

Option C is incorrect because DCF is versatile and can be applied to companies of various types, not just asset-heavy companies.

Option D is incorrect because DCF can be applied across industries, not exclusively to cyclical ones.

Thus, the correct answer is B. DCF analysis requires estimating future cash flows and an appropriate discount rate, both of which involve significant assumptions.

Question 3

In relative valuation, which of the following multiples is most appropriate for valuing a company in the technology sector that is currently experiencing high growth?

A. Price-to-Earnings (P/E) ratio

B. Price-to-Book (P/B) ratio

C. EV/EBITDA multiple

D. Dividend Yield

Answer: C. EV/EBITDA multiple

Explanation: The EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization) multiple is often preferred for high-growth sectors like technology because it provides a measure of operating profitability without being affected by capital structure, taxes, or non-cash accounting items like depreciation and amortization. Technology companies often have high growth rates and may reinvest profits back into the business rather than paying out dividends, making EV/EBITDA a more relevant metric for assessing their value.

- Option A (P/E ratio) can be challenging in high-growth sectors where earnings may be volatile or where companies may prioritize growth over immediate profitability.

- Option B (P/B ratio) is typically less relevant for technology companies, which may have significant intangible assets not reflected on the balance sheet. This ratio is more commonly used for asset-heavy industries.

- Option D (Dividend Yield) is not suitable for high-growth companies in the tech sector, as they often retain earnings for reinvestment rather than paying dividends.

Thus, the correct answer is C. EV/EBITDA multiple, as it better reflects the profitability and operating performance of high-growth companies in the tech sector.