Principles of Asset Allocation

Principles of Asset Allocation is a core topic in the CFA curriculum that focuses on how to strategically distribute investments across various asset classes to achieve a balance between risk and return. The objective is to optimize portfolio performance while considering an investor’s risk tolerance, time horizon, and financial goals. This topic explores the theoretical and practical foundations of asset allocation, offering insights into the use of diversification, correlation, and asset class characteristics to manage portfolio risk. Understanding these principles is essential for constructing portfolios that are aligned with investors’ long-term objectives.

Learning Objectives

In studying “Principles of Asset Allocation” for the CFA, you should learn to understand the foundational concepts of asset allocation and its role in achieving specific investment objectives. Analyze how different asset classes, such as equities, fixed income, and alternative investments, contribute to risk and return in a diversified portfolio. Evaluate the importance of investor risk tolerance, time horizon, and financial goals in the asset allocation process. Explore the use of models, including mean-variance optimization, to construct efficient portfolios that maximize returns for a given level of risk. Additionally, understand how asset allocation strategies can be adjusted for changing economic conditions and market environments, and recognize the impact of correlation between asset classes on portfolio performance.

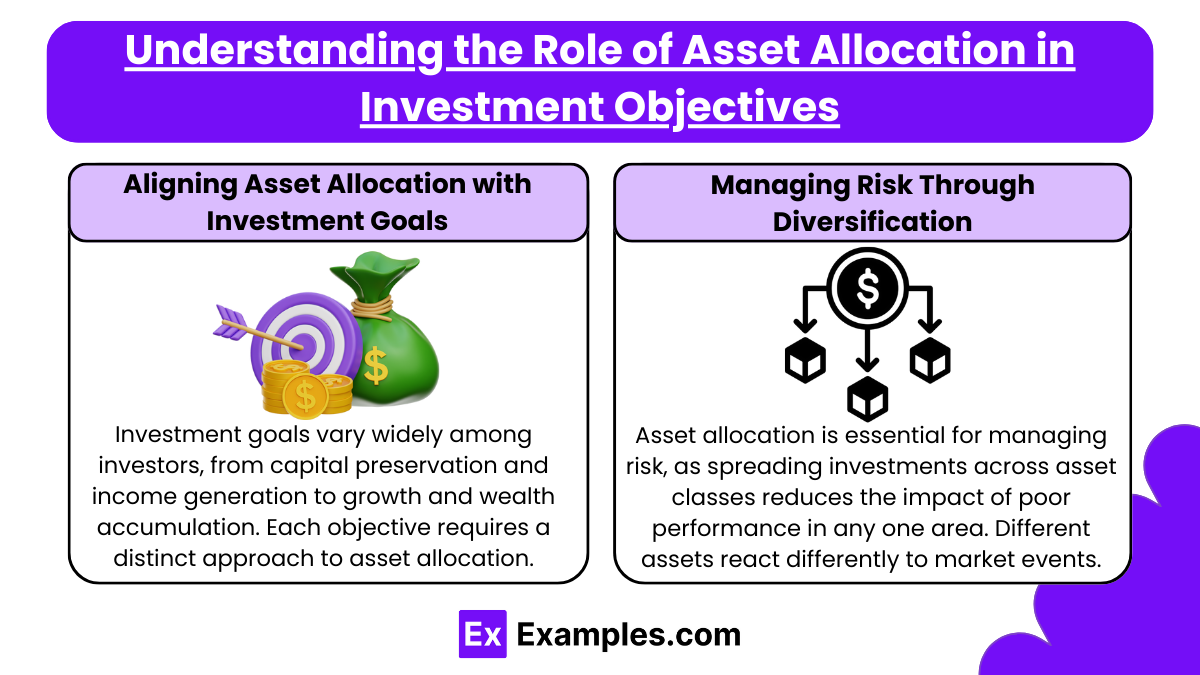

Understanding the Role of Asset Allocation in Investment Objectives

Asset allocation is the strategy of dividing investments among various asset classes—such as stocks, bonds, real estate, and cash—to achieve specific financial goals while managing risk. It is a key component of any investment strategy, as it influences both the potential returns and the level of risk associated with a portfolio. By aligning asset allocation with investment objectives, investors can enhance their chances of achieving their financial goals while navigating different market conditions. Here’s an in-depth look at how asset allocation plays a role in meeting investment objectives.

1. Aligning Asset Allocation with Investment Goals

Investment goals vary widely among investors, from capital preservation and income generation to growth and wealth accumulation. Each objective requires a distinct approach to asset allocation to balance risk and return effectively.

- Capital Preservation: For investors prioritizing capital preservation (e.g., those nearing retirement), asset allocation focuses on stability and minimal risk. Allocations lean heavily towards bonds, cash, and other low-volatility assets to safeguard the principal.

- Example: An investor with a short-term goal may allocate 70% to bonds, 20% to cash, and only 10% to stocks, reducing exposure to market fluctuations.

- Income Generation: Investors seeking regular income may allocate more to bonds, dividend-paying stocks, and real estate investments. These assets provide a steady income stream and are typically less volatile than growth-oriented equities.

- Example: A retiree may allocate 60% to bonds and 30% to dividend stocks, with 10% in real estate, balancing income with stability.

- Capital Growth: For long-term growth, investors may focus on stocks and equity-based investments. This strategy entails higher risk but offers potential for greater returns over time, making it suitable for younger investors or those with long investment horizons.

- Example: A young investor saving for retirement might allocate 80% to equities and 20% to bonds, maximizing growth potential over a long time horizon.

Key Takeaway: Tailoring asset allocation to investment goals helps optimize the portfolio for the desired outcome, whether it’s preserving wealth, generating income, or achieving growth.

2. Managing Risk Through Diversification

Asset allocation is essential for managing risk, as spreading investments across asset classes reduces the impact of poor performance in any one area. Different assets react differently to market events, providing a cushion during market volatility.

- Risk Reduction: Diversification across asset classes like stocks, bonds, and commodities lowers overall portfolio risk by combining assets with low or negative correlations.

- Example: In a diversified portfolio, stocks might decline during an economic downturn, while bonds or gold could perform better, stabilizing the portfolio.

- Balancing Volatility: Equities are generally more volatile but offer higher growth, while bonds and cash are less volatile but provide stability. Allocating a mix of these assets balances risk and return.

- Example: A balanced portfolio with 60% equities and 40% bonds moderates volatility while still offering growth potential, making it suitable for moderate-risk investors.

Key Takeaway: Asset allocation helps manage risk through diversification, reducing the likelihood of large losses and creating a more resilient portfolio.

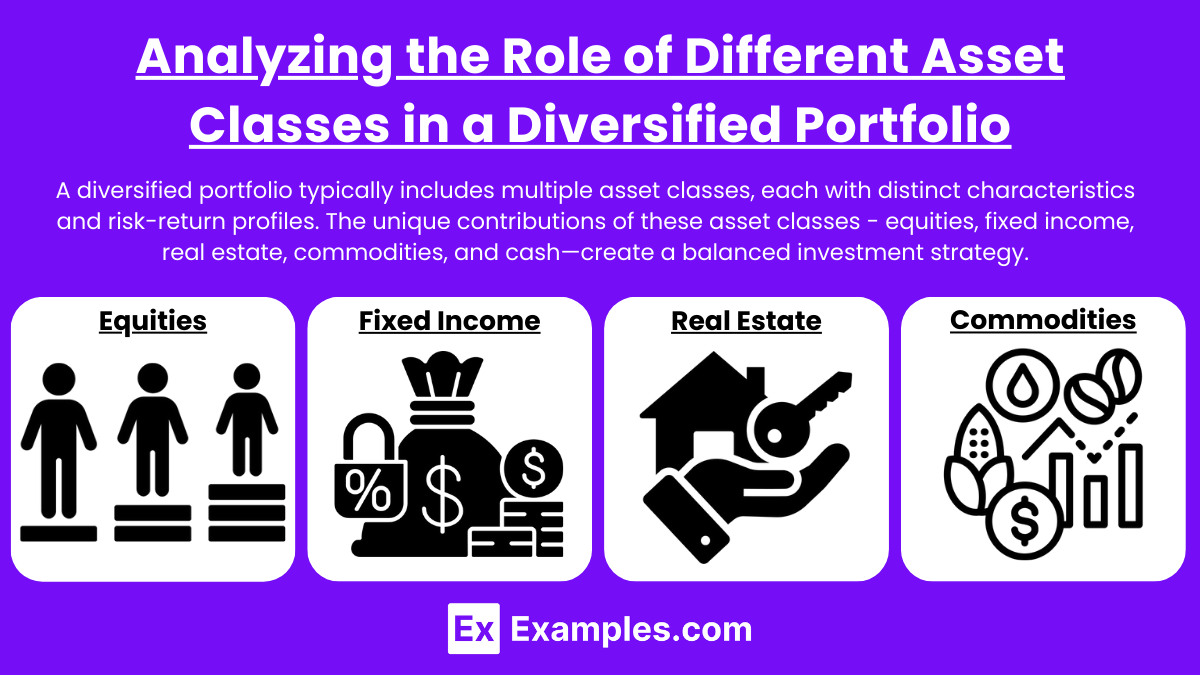

Analyzing the Role of Different Asset Classes in a Diversified Portfolio

A diversified portfolio typically includes multiple asset classes, each with distinct characteristics and risk-return profiles. The unique contributions of these asset classes—equities, fixed income, real estate, commodities, and cash—create a balanced investment strategy that helps mitigate risk, enhances potential returns, and supports long-term financial goals. Here’s an analysis of the role each major asset class plays in a diversified portfolio.

1. Equities (Stocks)

Equities are a high-growth asset class representing ownership in a company. They are generally the most volatile but offer significant potential for long-term capital appreciation, making them a core component of most growth-oriented portfolios.

- Role: Equities drive portfolio growth by delivering potentially high returns over time. They are essential for achieving long-term goals, such as retirement savings or wealth accumulation.

- Risk Profile: Equities are subject to market risk and can experience significant fluctuations, especially during economic downturns. However, over long periods, they tend to outperform other asset classes.

- Types of Equities:

- Large-Cap Stocks: Established companies with stable earnings, offering moderate growth with relatively lower risk.

- Small-Cap Stocks: Smaller, growth-focused companies with higher growth potential but more volatility.

- International Stocks: Exposure to global markets, helping diversify geographic risk and capture international growth opportunities.

Example: A young investor with a long-term goal may allocate 70-80% of their portfolio to equities to maximize growth potential.

2. Fixed Income (Bonds)

Fixed-income securities, such as bonds, offer predictable interest payments and typically lower risk than equities.

- Role: Bonds provide income and stability, offsetting the volatility of equities. They serve as a foundation for more conservative portfolios or for balancing risk in a growth-focused portfolio.

- Risk Profile: Bonds are less volatile than stocks but sensitive to interest rate changes and credit risk. Government bonds are among the safest, while corporate and high-yield bonds carry more risk and return potential.

- Types of Bonds:

- Government Bonds: Highly stable, suitable for conservative investors.

- Corporate Bonds: Offer higher yields with moderate risk, ideal for those seeking income.

- Municipal Bonds: Provide tax advantages in certain regions, attractive for high-income investors.

Example: An investor nearing retirement might allocate 40-50% of their portfolio to bonds, prioritizing stability and regular income.

3. Real Estate

Real estate provides diversification through physical property investments or real estate investment trusts (REITs), adding a tangible asset class that often acts as an inflation hedge.

- Role: Real estate contributes steady income through rental yields and has potential for capital appreciation. It can act as a hedge against inflation and economic volatility, often moving independently of stocks and bonds.

- Risk Profile: Real estate investments carry specific risks, including market liquidity, property maintenance, and economic cycles. However, they also offer stability and tend to have low correlation with equities.

- Types of Real Estate Investments:

- Physical Properties: Direct investment in real estate, providing control and potential income.

- REITs: Publicly traded, providing exposure to real estate without direct ownership, with liquidity similar to stocks.

Example: An investor seeking diversification and passive income might allocate 10-20% of their portfolio to real estate, balancing risk and growth potential.

4. Commodities

Commodities, such as gold, oil, and agricultural products, provide diversification and inflation protection by adding a tangible asset class to a portfolio.

- Role: Commodities serve as a hedge against inflation and economic uncertainty. They often perform well during inflationary periods when other asset classes, such as bonds, may decline in real value.

- Risk Profile: Commodities are volatile, influenced by global supply and demand dynamics, geopolitical events, and currency fluctuations. However, they add resilience to a portfolio when other assets struggle.

- Types of Commodities:

- Precious Metals: Gold and silver are popular choices for stability in times of economic distress.

- Energy: Oil and natural gas, highly sensitive to geopolitical conditions.

- Agricultural Products: Wheat, corn, and livestock, offering exposure to the food supply sector.

Example: An investor concerned about inflation or economic instability might allocate 5-10% of their portfolio to commodities, especially in inflationary periods.

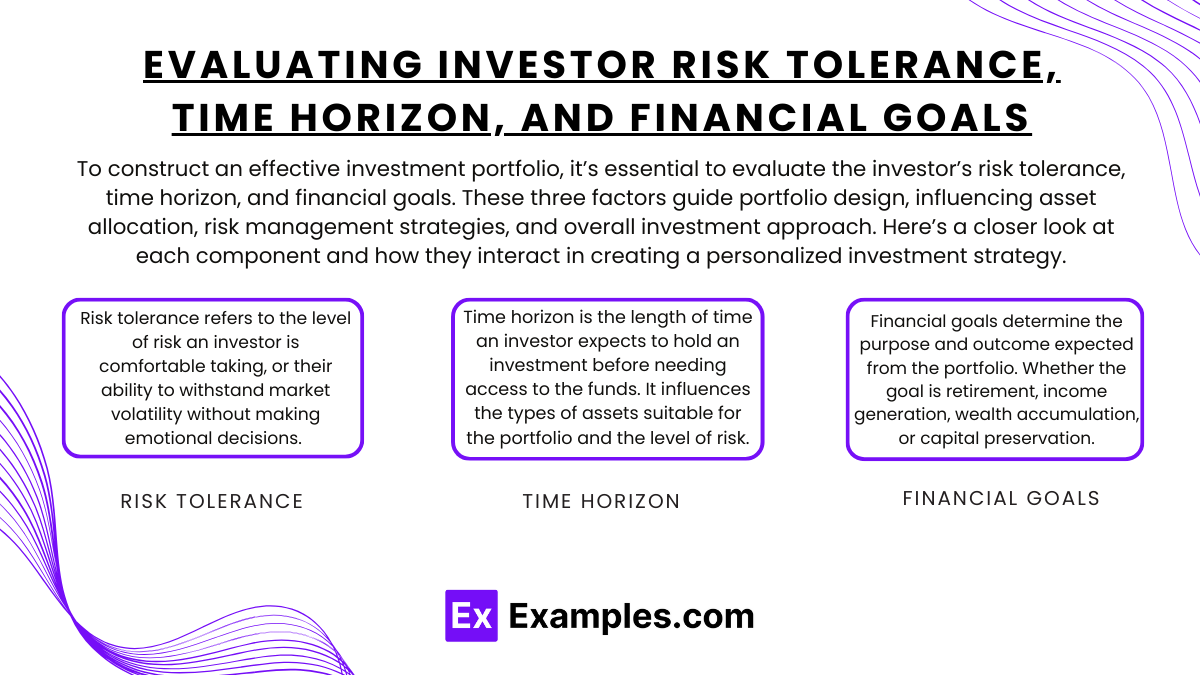

Evaluating Investor Risk Tolerance, Time Horizon, and Financial Goals

To construct an effective investment portfolio, it’s essential to evaluate the investor’s risk tolerance, time horizon, and financial goals. These three factors guide portfolio design, influencing asset allocation, risk management strategies, and overall investment approach. Here’s a closer look at each component and how they interact in creating a personalized investment strategy.

1. Risk Tolerance

Risk tolerance refers to the level of risk an investor is comfortable taking, or their ability to withstand market volatility without making emotional decisions. It is influenced by personal factors such as age, financial knowledge, income stability, and psychological disposition. Risk tolerance typically falls into three main categories:

- Conservative: Conservative investors prefer stability and are less comfortable with volatility. They aim to preserve capital and accept lower returns for reduced risk, often favoring fixed-income securities and low-volatility assets.

- Example: A conservative investor might have a portfolio with 70% bonds and 30% equities, focusing on capital preservation.

- Moderate: Moderate investors are willing to take some risk for potential growth. They seek a balanced portfolio that combines stability with growth opportunities, often with a balanced mix of equities and bonds.

- Example: A moderate investor may hold a 60/40 split between equities and bonds, balancing growth with risk mitigation.

- Aggressive: Aggressive investors have a high tolerance for risk, seeking maximum returns and accepting significant volatility. They typically invest heavily in equities and high-growth assets, focusing on capital appreciation over time.

- Example: An aggressive investor might allocate 80-90% to equities, aiming for substantial growth despite short-term market fluctuations.

Assessing Risk Tolerance: Risk tolerance is often assessed through questionnaires and discussions, exploring factors such as how the investor reacts to market downturns, their investment experience, and their comfort with potential losses. Understanding risk tolerance ensures the portfolio aligns with the investor’s psychological and financial capacity to handle volatility.

2. Time Horizon

Time horizon is the length of time an investor expects to hold an investment before needing access to the funds. It influences the types of assets suitable for the portfolio and the level of risk that can be tolerated. Generally, longer time horizons allow for greater risk-taking, as there is more time to recover from market downturns.

- Short-Term Horizon (1-3 Years): Investors with short time horizons prioritize stability and liquidity, focusing on preserving capital over growth. Portfolios may consist of cash equivalents, short-term bonds, and other low-risk assets.

- Example: An investor saving for a house down payment in two years may allocate 80% to cash and 20% to short-term bonds, avoiding high-volatility assets like stocks.

- Medium-Term Horizon (3-10 Years): For medium-term goals, investors may balance growth with stability, including a mix of stocks and bonds. This approach allows for moderate growth while managing volatility.

- Example: An investor saving for a child’s college fund over 8 years might have a 50/50 allocation between stocks and bonds, providing growth potential with some stability.

- Long-Term Horizon (10+ Years): Long time horizons support higher equity allocations, as investors can weather market fluctuations. Portfolios may focus on growth-oriented assets like equities and real estate.

- Example: A 30-year-old saving for retirement in 30 years may allocate 80-90% of their portfolio to equities, maximizing growth potential.

Assessing Time Horizon: Understanding time horizon helps set realistic expectations for returns and guides the selection of assets with appropriate risk levels. As investors near their goals, they often adjust the portfolio to reduce risk and ensure the funds will be available when needed.

3. Financial Goals

Financial goals determine the purpose and outcome expected from the portfolio. Whether the goal is retirement, income generation, wealth accumulation, or capital preservation, it guides the asset allocation strategy, helping to select investments that support specific objectives.

- Wealth Accumulation (Growth-Oriented Goals): For investors focused on growing their wealth, the portfolio may have a higher allocation to equities and other high-growth assets. Long-term goals like retirement and generational wealth building usually involve growth-focused strategies.

- Example: A young professional building wealth might hold a growth-oriented portfolio with 80% stocks and 20% bonds, prioritizing long-term appreciation.

- Income Generation: Investors seeking income generation often prioritize assets that provide regular payouts, such as dividend stocks, bonds, and real estate. This strategy suits investors who rely on their portfolio to meet living expenses or supplement income.

- Example: A retiree may allocate 40% to bonds, 30% to dividend stocks, and 30% to real estate investments, creating a diversified income stream.

- Capital Preservation: For goals focused on preserving capital, such as emergency funds or short-term savings, portfolios consist mainly of cash and bonds to avoid volatility and maintain liquidity.

- Example: An investor preserving capital for near-term needs may hold 90% in cash equivalents and 10% in bonds, focusing on security and easy access.

- Specific Goals (e.g., College Savings, Home Purchase): Investors may also have unique goals, such as saving for education or purchasing a property. Portfolios for specific goals align with the time horizon and risk tolerance relevant to the purpose.

- Example: A parent saving for a child’s college fund over 15 years might start with a high equity allocation for growth, gradually shifting to bonds as the goal date approaches.

Assessing Financial Goals: Identifying and prioritizing financial goals ensures that the portfolio is tailored to the investor’s specific needs. This alignment provides clarity, helping investors stay focused on their objectives and adjust strategies as their financial situation evolves.

Exploring Models for Constructing Efficient Portfolios

Efficient portfolio construction is the process of selecting assets in a way that maximizes returns for a given level of risk or minimizes risk for a target return. Several models help achieve these goals by optimizing the asset allocation based on mathematical principles and risk-return analysis. The most popular models include Modern Portfolio Theory (MPT), Capital Asset Pricing Model (CAPM), Arbitrage Pricing Theory (APT), and Black-Litterman Model. Each model offers a unique perspective on constructing portfolios, considering various risk factors and return expectations. Here’s a breakdown of these models and how they contribute to efficient portfolio construction.

1. Modern Portfolio Theory (MPT)

Modern Portfolio Theory (MPT), developed by Harry Markowitz, is the foundation of portfolio optimization. It suggests that an efficient portfolio is one that provides the highest possible return for a given level of risk or the lowest possible risk for a given return. The main goal of MPT is to build a diversified portfolio that minimizes overall portfolio risk by combining assets with varying correlations.

Key Concepts:

- Expected Return: The weighted average of the individual asset returns based on historical performance.

- Risk (Standard Deviation): A measure of volatility or the deviation of returns from the expected return.

- Correlation: The relationship between the returns of different assets, which is central to diversification.

- Efficient Frontier: MPT introduces the concept of the efficient frontier, a curve representing portfolios that offer the highest expected return for each level of risk. Portfolios on the efficient frontier are considered “efficient,” while those below it are suboptimal.

- Limitations: MPT relies heavily on historical data, assumes that asset returns are normally distributed, and does not account for all types of risks. Additionally, it assumes that all investors are rational and risk-averse, which may not always hold true in real markets.

Example: An investor might use MPT to allocate 60% to stocks, 30% to bonds, and 10% to commodities, optimizing for maximum returns while staying within a moderate risk tolerance.

2. Capital Asset Pricing Model (CAPM)

The Capital Asset Pricing Model (CAPM) builds on MPT and introduces a way to measure the expected return of an asset in relation to its risk compared to the overall market. CAPM asserts that an asset’s return should equal the risk-free rate plus a premium for taking on additional risk.

Key Components:

- Risk-Free Rate: The return on an investment with zero risk, often represented by government bond yields.

- Market Risk Premium: The difference between the expected return of the market and the risk-free rate, compensating investors for taking on additional risk.

- Beta (β): A measure of an asset’s volatility relative to the market. A beta of 1 means the asset moves with the market; greater than 1 means it’s more volatile, and less than 1 means it’s less volatile.

- Expected Return Calculation: CAPM calculates the expected return of an asset as: Expected Return = Risk-Free Rate+β×(Market Return−Risk-Free Rate)

- Application: CAPM helps investors assess whether an asset offers a sufficient return for its level of risk. Portfolios are constructed based on each asset’s beta, choosing assets with returns that justify their risk.

- Limitations: CAPM assumes a single-period investment horizon, market efficiency, and a static risk premium, which may not align with real-world conditions. It also relies on beta, which may not fully capture an asset’s risk.

Example: An investor using CAPM might select assets with higher expected returns based on their beta, creating a portfolio that aligns with their risk tolerance and market expectations.

3. Black-Litterman Model

The Black-Litterman Model, developed by Fischer Black and Robert Litterman, combines MPT with investors’ personal market views to create optimized portfolios. It improves upon traditional mean-variance optimization by blending market equilibrium returns with the investor’s subjective views on asset returns.

Key Components:

- Market Equilibrium Returns: The model starts with the assumption of market equilibrium, where asset returns are in line with market expectations.

- Investor Views: Investors can input their own views on expected returns for specific assets, which are then combined with equilibrium returns to create a balanced forecast.

- Bayesian Approach: Black-Litterman uses a Bayesian approach to adjust the weights of assets, considering both market consensus and personal beliefs. This results in a more stable and realistic portfolio that mitigates issues like overconcentration in highly volatile assets.

- Application: The model is widely used by institutional investors and portfolio managers who have unique insights about market trends and wish to incorporate these views into portfolio construction.

- Limitations: The Black-Litterman model is mathematically complex, requiring advanced statistical and financial knowledge. It also assumes accurate market equilibrium and investor views, which may not always hold true.

Example: An investor may use the Black-Litterman model to overweight specific sectors based on their own positive outlook, such as technology or healthcare, while still maintaining the overall balance suggested by market equilibrium.

Examples

Example 1: Risk Tolerance Assessment

One of the fundamental principles of asset allocation is understanding an investor’s risk tolerance. This involves evaluating how much risk an investor is willing and able to take based on their financial situation, investment goals, and time horizon. For instance, a young investor with a long time frame may have a higher risk tolerance and allocate more to equities, while a retiree may prefer a conservative approach with more bonds to preserve capital.

Example 2: Diversification Across Asset Classes

Diversification is a key principle in asset allocation that involves spreading investments across various asset classes, such as stocks, bonds, real estate, and cash. This strategy helps to reduce risk since different asset classes often respond differently to market conditions. For example, during a stock market downturn, bonds may provide stability and income, thus balancing overall portfolio performance.

Example 3: Strategic vs. Tactical Allocation

Asset allocation can be categorized into strategic and tactical approaches. Strategic asset allocation involves setting a long-term target mix of asset classes based on expected returns and risk levels. In contrast, tactical asset allocation allows for short-term adjustments based on market conditions or economic outlooks. For example, an investor may increase equity exposure during a bull market while reallocating to bonds during periods of economic uncertainty.

Example 4: Rebalancing the Portfolio

Regularly rebalancing an investment portfolio is another important principle of asset allocation. Over time, asset values change, which can lead to a shift in the originally intended allocation. For instance, if equities outperform bonds significantly, the portfolio may become more equity-heavy than desired. Rebalancing involves selling some of the outperforming assets and buying underperforming ones to return to the target allocation, thereby maintaining the desired risk profile.

Example 5: Consideration of Time Horizon

The investment time horizon plays a crucial role in determining asset allocation. Longer time horizons generally allow investors to take on more risk, as they have more time to recover from market fluctuations. For example, a young investor saving for retirement in 30 years might allocate a significant portion of their portfolio to growth-oriented assets like stocks. Conversely, someone planning to make a withdrawal in the near future, such as a home purchase, would likely allocate a larger portion to more stable, income-producing assets like bonds or cash equivalents to minimize risk.

Practice Questions

Question 1

What is the primary objective of asset allocation in an investment portfolio?

A) To maximize returns at all costs

B) To minimize taxes on investment income

C) To balance risk and return according to an investor’s goals

D) To invest in a single asset class for simplicity

Correct Answer: C) To balance risk and return according to an investor’s goals.

Explanation: The primary objective of asset allocation is to create a balance between risk and return that aligns with the investor’s financial goals, risk tolerance, and investment horizon. Proper asset allocation helps manage risk by diversifying investments across different asset classes, allowing for the potential of higher returns while mitigating the impact of market volatility. Options A and D are incorrect because they do not address the fundamental principles of risk management and diversification. Option B, while relevant, does not encompass the broader objective of asset allocation.

Question 2

Which of the following best describes the principle of diversification in asset allocation?

A) Investing in as many different securities as possible without regard to asset class.

B) Spreading investments across different asset classes to reduce overall risk.

C) Focusing solely on high-risk investments for greater returns.

D) Allocating all funds to cash equivalents for safety.

Correct Answer: B) Spreading investments across different asset classes to reduce overall risk.

Explanation: Diversification involves spreading investments across various asset classes (such as stocks, bonds, real estate, and commodities) to minimize risk. By diversifying, investors can reduce the impact of poor performance in any single asset class, thereby enhancing the overall stability of their portfolio. Option A does not emphasize the importance of asset classes, while options C and D contradict the principle of diversification by either concentrating risk or avoiding growth opportunities.

Question 3

How often should an investor consider rebalancing their portfolio to maintain the desired asset allocation?

A) Only when market conditions change dramatically

B) Once every five years

C) Regularly, based on a set schedule or after significant performance changes

D) Never, once the initial allocation is set

Correct Answer: C) Regularly, based on a set schedule or after significant performance changes.

Explanation: Regular rebalancing is essential to maintain the target asset allocation in an investment portfolio. This process involves adjusting the portfolio back to its intended allocation after significant performance changes or at regular intervals (e.g., annually or semi-annually). Failure to rebalance can lead to unintended risk exposure as certain asset classes may outperform others over time, shifting the original allocation. Options A, B, and D suggest infrequent or no rebalancing, which can undermine the effectiveness of asset allocation strategies.