Manufacturers of products have a lot to take care of financially in comparison to service providers. Though all businesses deal with variable and fixed costs, the weekly, monthly, and annual breakdown of a manufacturer’s spendings is far more complicated than other lines of business. Unlike service providers and retailers, manufacturers calculate the work in process’s payments, while accounting the actual cost that consists of payments for direct labor, inventory of raw materials, equipment, and more. Despite all the complexities, making a budget document for them is quite simple. If you’re eager to know how, read our article and browse through our variety of examples below!

[bb_toc content=”][/bb_toc]

10+ Manufacturing Budget Examples

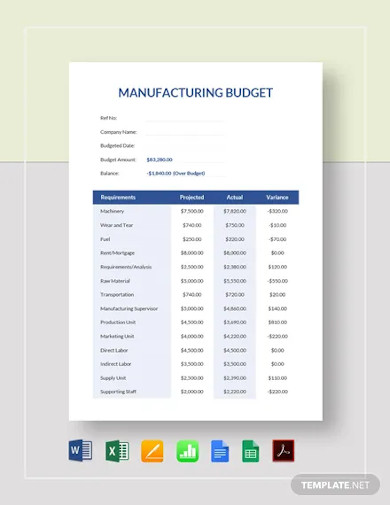

1. Manufacturing Budget Template

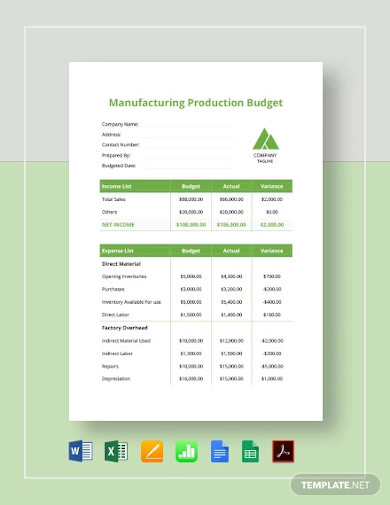

2. Manufacturing Production Budget Template

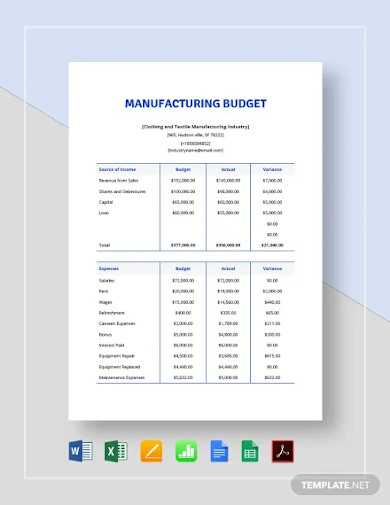

3. Manufacturing Company Budget Template

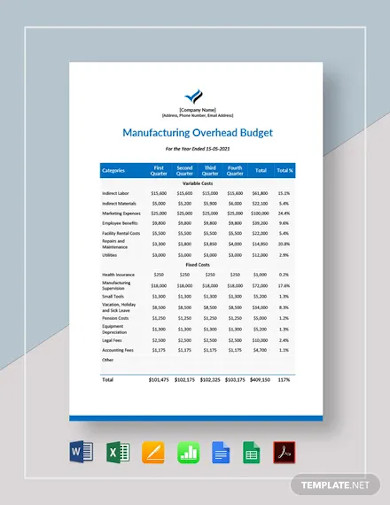

4. Manufacturing Overhead Budget Template

5. Free Manufacturing Budget Template

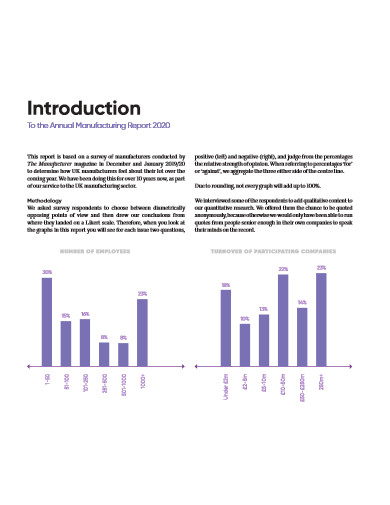

6. Annual Manufacturing Budget Report

7. Manufacturing Budget and Accounting

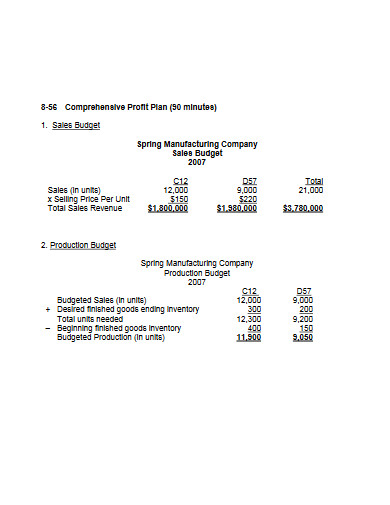

8. Manufacturing Company Sales Budget

9. Manufacturing Budgeting in PDF

10. Manufacturing Budget Example

11. Sample Manufacturing Budget

What Is a Manufacturing Budget?

A manufacturing budget is a document that presents the complete list of items used in the manufacturing of goods. These items go together with their corresponding value. According to tutor2u, the budget serves many purposes. To name a few, they said that such a document sets priorities and targets, guides stakeholders to fulfill objectives, and distributes responsibilities and resources fairly. Aside from that, the same source cited that they encourage staff to improve their efficiency, help monitor their performances, and, ultimately, manage income and expenditure. Through the aforementioned functionalities, the budget is, without a doubt, a necessary element to a manufacturing company’s success.

Fixed Cost V.S. Variable Cost

Business costs have two categories – fixed costs and variable costs. Fixed costs describe the expenses that remain consistent regardless of how high or low the volume of produced goods is. Good examples of this type of cost include rents, internet billings, insurance, loan payments, or employee salaries. Because these costs stay the same throughout the fiscal year, anyone can say that they are easier to budget. On the other hand, variable costs vary on the usage of materials, equipment, and other resources to produce a certain volume of goods. Examples of these are direct labor, taxes, commissions, and other manufacturing expenses. Because of such costs’ dependence on the output level, managers can easily manipulate them to their advantage.

How To Create a Manufacturing Budget

Creating a company budget requires knowledge and understanding of the standards, from the set of sections to the incorporation of technical writing principles. If you lack those, then there’s no need to worry because we have our standardized outline and insights ready to guide you.

1. Describe Goals

Start your budgeting process by describing what your short-term and long-term goals are. Doing so is important, so the intended audience can understand the document’s purpose. The budget can go in two different ways. First, you can use it as a financial proposal to get the much-needed fundings for your manufacturing operations. Second, you can use it to ensure that your manufacturing stakeholders do not fall short financially on or off their work schedule.

2. Present Income

Income plays a very important role in budgeting. In fact, it is the most important element in a budget document. It is the basis of the sections that come right after this. Presenting it may vary depending on your purpose. If you’re using it as a proposal, you can write down a realistic prediction of the numbers and figures. To do so, you may have to look back on past financial reports, profit and loss statements, cash flow statements, and your company’s investment portfolio. If you’re using it to keep track of your manufacturing department’s financial health, use your current data.

3. Identify Fixed Costs

Another important element of your budget document is your company’s fixed costs, whose inclusions are already mentioned above. The calculation of its entries should be accurate to avoid confusion. But for you to easily do so, you must consider getting the complete list of fixed costs items, their corresponding taxes, interests, depreciation, and amortizations.

4. Determine Variable Costs

Just like fixed costs, you should note down the complete details of the variable costs too. Apart from the thorough list of raw materials, equipment, and direct labor, you also have to give out the fact-based amounts together with the exact volume of goods that your company is planning to produce.

5. Distribute Income Accordingly

Now that you have both the fixed costs and variable costs in place, organize them according to their importance in the manufacturing process. After doing so, distribute the income amount to each item in the catalogs. Make sure that the income is fairly distributed and that the costs do not go beyond it. If the expenditures exceed the income, you have to redo your allocation or submit a request letter to your executives to appeal for additional monetary assistance.

FAQs:

What are some of the risks that budgeting brings?

– Making budgets without going through proper negotiation can demotivate stakeholders and their members

– The unrealistic setting of goals can also demotivate employees

– Company departments will fight over the budget allocation

– Employees think that unused budget will go to waste

– Budgets are reserved for big projects, forgetting the importance of the smaller ones

Does budgeting have limitations?

Yes, it does. Some of its limitations are the following:

– Budgets should be based on historical data. Inaccurate assumptions will make your budget unrealistic.

– Budgets limit executives’ decision-making authority.

– Budgets should accord with the sudden changes.

– Budgets are not so good for long-term goals.

What is budget variance?

The budget variance is the difference between your company’s budget amount and the actual amount of spendings. It can either be shortage or excess.

As mentioned before, manufacturing’s financial aspect is complicated, especially budgeting. But through the standards set by both past and current societies, it transforms into a more manageable one. In her book entitled Life & Debt: A Fresh Approach to Achieving Financial Wellness, debt relief lawyer and debt expert Leslie Tayne quoted that, “Budgeting has only one rule: Do not go over budget.” These words only mean that successful budgeting is simply the setting of expenses not greater than the earnings of a certain company. Then again, a lot of factors have to be taken into account, making your decision-making skills just as important as any rule.